Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER STAPLES

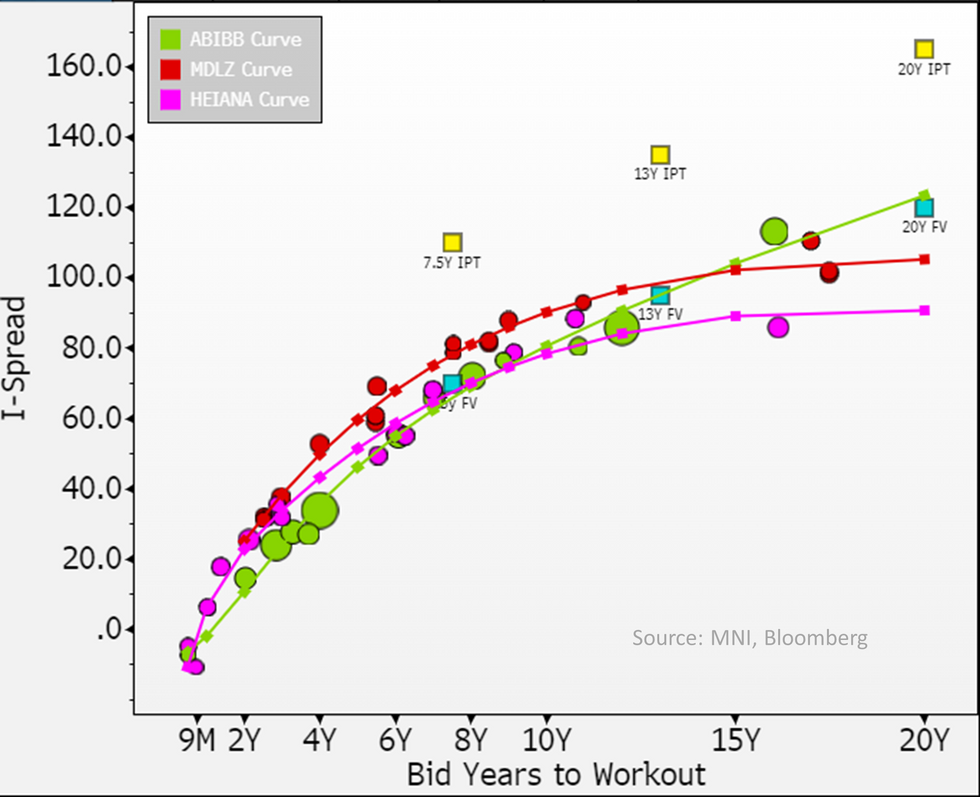

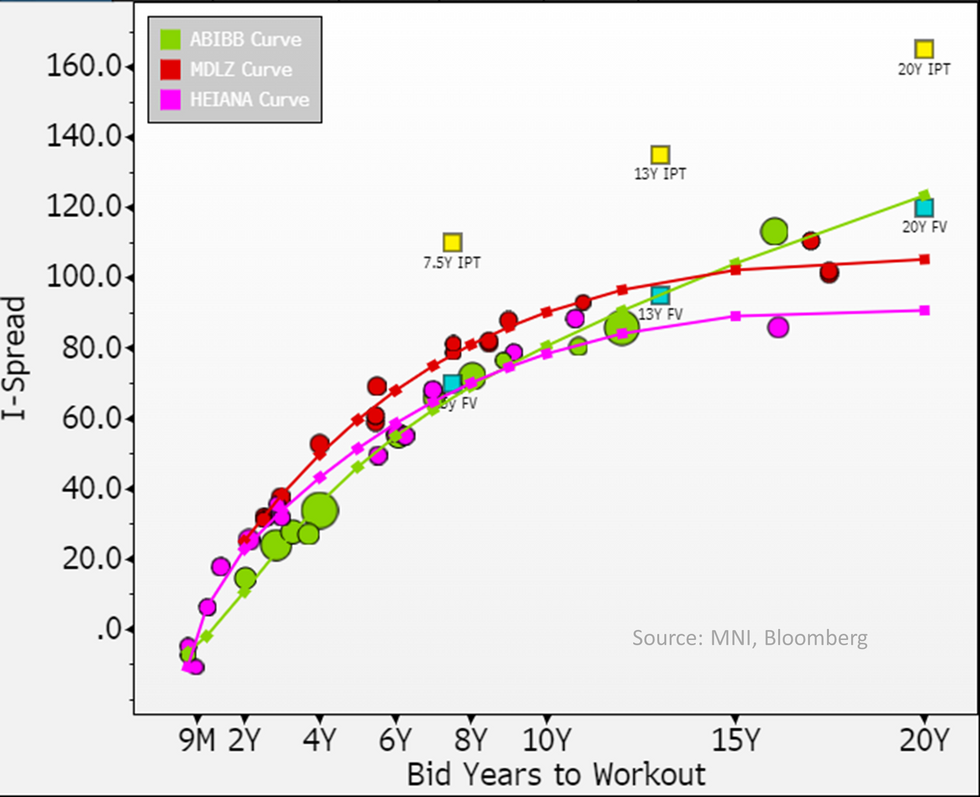

We see FV (vs. IPT) at +70 (+110), +95 (+135), +120 (+165).

- Re. the 20's; the longest in Euro F&B similar rated space are the March & Sept 41's from Mondalez (A, BBB) at ~ +105 but trading at low cash prices <€70 - not useful as bnchmark.

- Outside F&B names, we think Booking.com 44's (new issues) are a ceiling at +136bps & spread our FV -16bps to it - we've spread it wider vs. 36's trading -24 tighter given ABIBB 40's is moving wider/away from curve this morning.

- Re. ratings; it received a one-notch upgrade last year from both majors into A3/A- & trades in-line with this - we don't see any rating risk in either direction (leverage fell from 3.5* to 3.4* yoy as Moody's wanted/expected).

Recent 20Y/2044 €IG Supply (all in multi-part deals, Engie/booking most recent)

- €600m Engie (Baa1/BBB+); -25bps from IPT to price at +160; books skewed to 12Y/36's

- €750m Booking.com (A3/A-); -30bps to price at +165, books skewed towards it

- €1.5b Siemens (Aa3/AA-); -37bps to price at +103, books skewed towards it

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok