Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

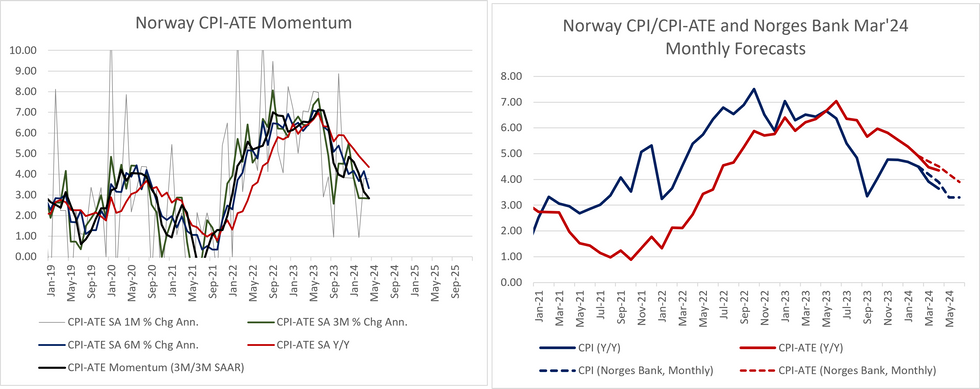

Norwegian April inflation exceeded consensus expectations, with CPI-ATE at 4.4% Y/Y (vs 4.2% cons, 4.5% prior) and 0.9% M/M NSA (vs 0.8% cons, 0.2% prior). Headline CPI was 3.6% Y/Y (vs 3.5% cons, 3.9% prior).

- The readings remain below the Norges Bank’s March MPR projections, but the CPI-ATE forecast error falls to 0.1pp from 0.2pp. The Bank had projected CPI-ATE at 4.5% Y/Y and CPI at 3.9% in April.

- Food prices rose 3.3% M/M, which appears to be a driver of the firmer than expected print, with analysts citing uncertainty over whether food prices would rebound after beginning the year on a weak note.

- Taken alone, the reading supports the Norges Bank’s hawkish tilt at the March meeting but will need to be taken alongside the May inflation figure to determine any impact on the June meeting guidance. NOK has strengthened on release, with NOKSEK trading above parity at typing.

- However, inflation momentum continued to moderate in April, with 3m/3m SAAR CPI-ATE at 2.84% (vs 3.17% prior), indicating that the wider disinflation process remains intact.

- Looking at the major sub-components, services inflation excluding rent moderated to 4.5% Y/Y (vs 5.0% prior) while consumer goods eased to 4.1% (vs 4.3% prior).

- Breaking down consumer goods, domestic goods accelerated to 5.9% Y/Y (vs 5.8% prior) while imported goods were 3.4% (vs 3.6% prior).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok