Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

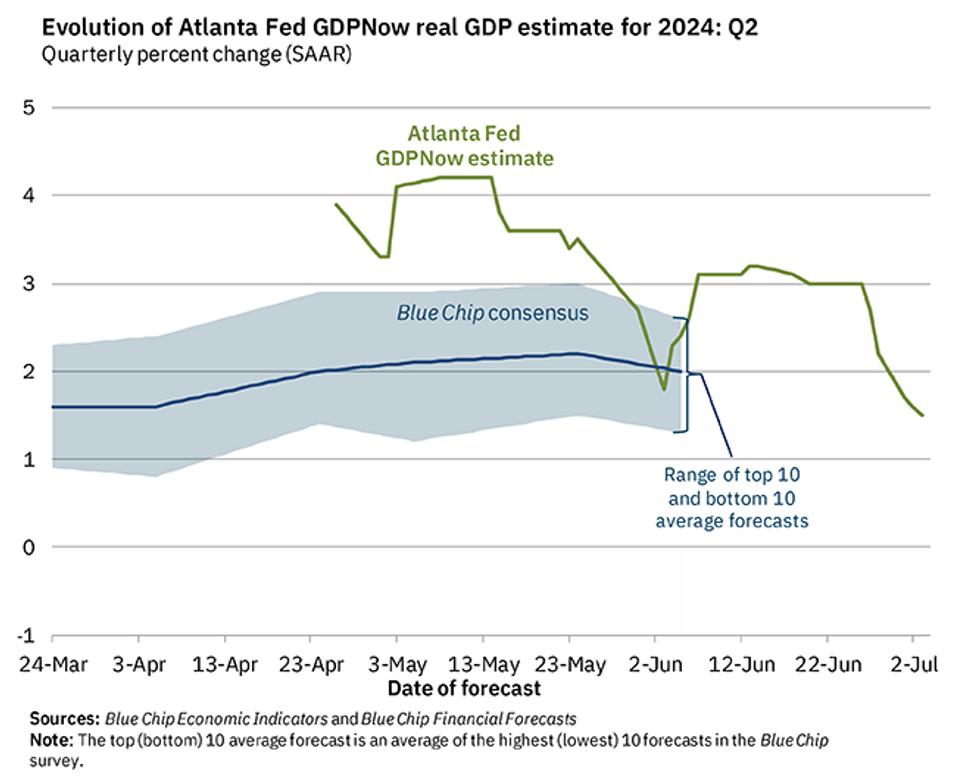

- The Atlanta Fed’s GDPNow for Q2 has continued its string of recent downgrades, most recently being cut to 1.55% from 1.7% two days ago, 2.2% after monthly PCE, 2.7% at Thursday’s GDP update and 3.0% from Jun 20.

- It’s a fresh low for the Q2 vintage and leaves GDP growth set for almost no acceleration from the 1.4% seen in Q1.

- Forecasts for real consumption have been cut again from 1.5% to 1.1% (from 2.5% last week), whilst real gross private domestic investment has been trimmed from 6.9% to 6.5% (and from 8.8% last week).

- There is a small offsetting upward revision from a reduced net export drag of -0.78pps vs -0.94pps.

- Consumption is seen adding 0.76pp to GDP growth, a deceleration after the 1.0pp contribution in Q1.

- Changes in inventories still provide a large driver on the quarter, shifting from -0.4pp in Q1 to an assumed +0.7pp.

Source: Atlanta Fed

Source: Atlanta Fed

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok