Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

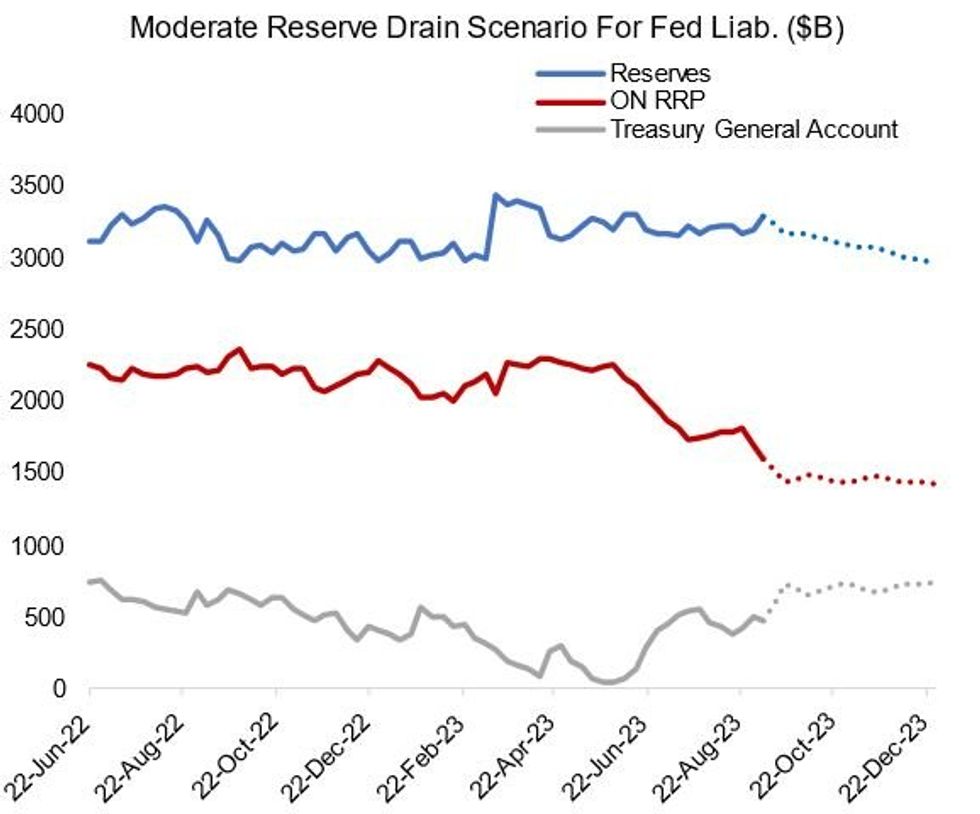

Perhaps the most remarkable turn in the Fed's balance sheet in the past month has been in overnight reverse repo levels which dropped $91B in the past week and $191B in the month to Sep 6th, to a post-March 2022 low $1.61T. At the same time bank reserves are up $94B on the week/$62B on the month despite a $49B rise in the Treasury General Account over the past month.

- The TGA’s post-debt limit cash rebuild in other words has gone as smoothly as could be expected so far, and broadly speaking in line with the “moderate” reserve drain scenario for Fed liabilities that we laid out a couple of months ago.

- The drop in ON RRP usage since June has come alongside some further gains in money market fund assets under management and steady commercial bank deposits. Certainly we’re not seeing any meaningful sign of reserve scarcity (eg bank deposit rates on offer, repo rates, Fed funding facility usage (including BTFP), and borrowing from FHLBs).

- Though as we have been saying, the real test for reserve scarcity would be going into late September and Q4, with QT continuing unabated and Treasury issuance picking up again with the TGA’s end-Sep cash balance target of $650B representing a $170B jump from current levels.

- By the end of next week TGA levels should be back over $600B and could exceed $700B temporarily later in the month. Levels could recede through early October as net bill supply pulls back but rise again by end-year Treasury is targeting an end-December $700B cash balance.

Source: MNI Estimates (Dotted Lines), Fed

Source: MNI Estimates (Dotted Lines), Fed

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok