Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

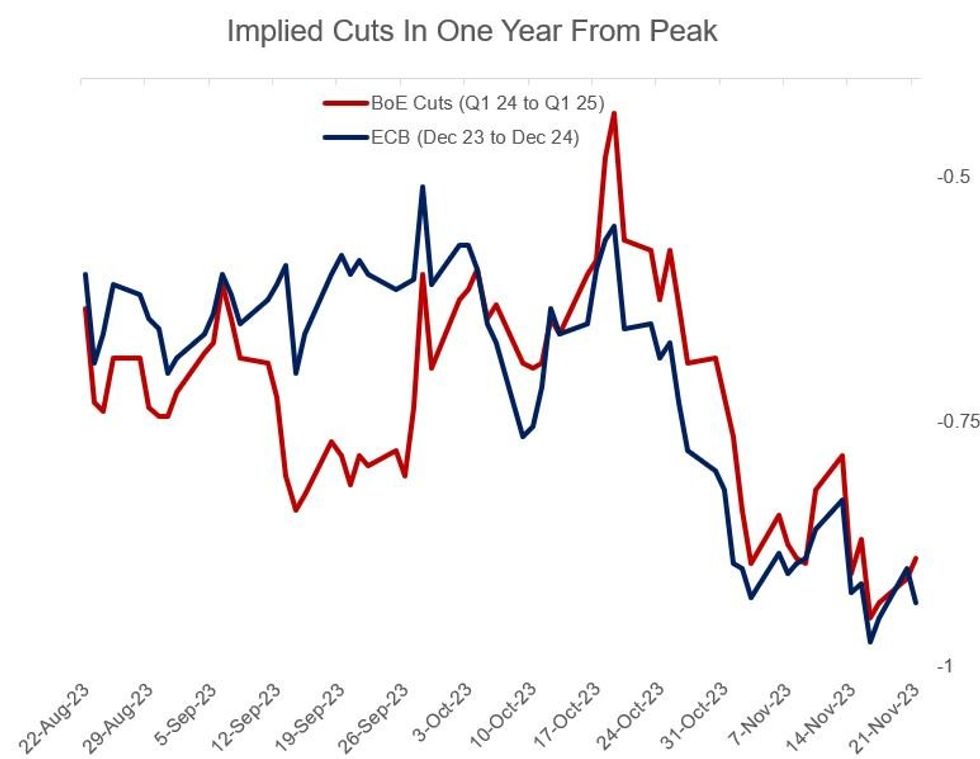

Tuesday saw a subtle shift in market pricing for cuts, with the ECB seen cutting a little more and the BoE a little less beyond their respective peaks.

- Hike pricing was unchanged as has become the norm (BoE Bank Rate seen peaking in Feb 2024 after 2-3bp more hikes, ECB is unequivocally finished per market pricing, with a Dec 2023 peak at around current levels).

- But today's session saw 2bp removed from BoE cumulative cuts in the year following the peak, with 89bp now seen through Feb/Mar 2025; around 4bp more cuts were priced into the ECB path however, with 94bp in reductions now seen in 2024.

- Both of those magnitudes are within the rough range they've been trading in since the middle of last week.

- Setting a dovish tone for the session, ECB's Villeroy downplayed the "last-mile" on inflation; BoE speakers including Gov Bailey didn't have much new to say but the reiteration of the higher-for-longer narrative plus fiscal uncertainty over the UK's Autumn Statement to be released tomorrow may have contributed to rate weakness.

- The first full 25bp BoE cut is seen only by August, a little later than the June MPC which has recently been the focus (though that's still over 90% cumulative probability as the first cut). The first full 25bp ECB cut is still seen by June.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok