Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

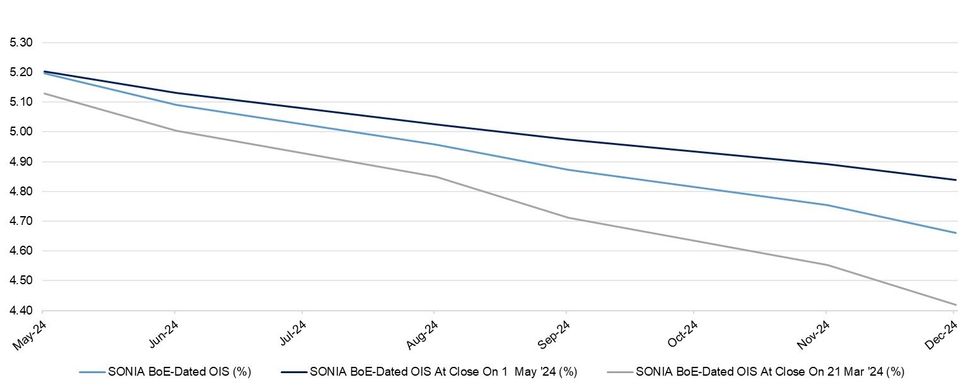

A visualisation of the swings in BoE-dated OIS pricing through the end of ’24 in the time since the March MPC can be seen below.

- Pricing is comfortably off extremes, albeit a little closer to the hawkish boundary than the dovish boundary,

- BoE-dated OIS shows close to 25bp less easing through year end than at the close that followed the March MPC.

- Repricing surrounding the U.S. Fed has been a major factor, with sporadic activity surrounding UK data releases and a dovish round of commentary from BoE Deputy Governor Ramsden also seen in that window.

- Our full preview of the impending BoE decision can be found here.

- On Wednesday we suggested that a dovish BoE outcome probably presents the greatest risk to current market pricing, although the move away from recent hawkish extremes provides a little more balance to the risk profile heading into the decision (click for more).

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| May-24 | 5.196 | -0.4 |

| Jun-24 | 5.090 | -11.0 |

| Aug-24 | 4.958 | -24.2 |

| Sep-24 | 4.873 | -32.7 |

| Nov-24 | 4.754 | -44.6 |

| Dec-24 | 4.662 | -53.8 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok