Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

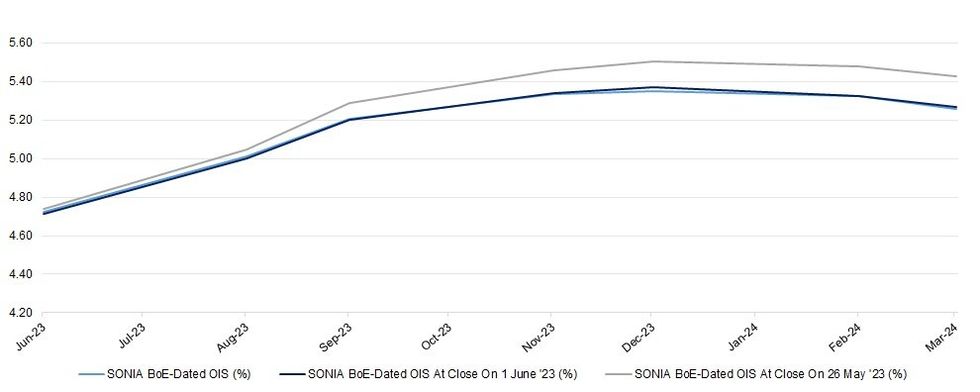

BoE-dated OIS is little changed on the session as we work towards the weekend, with little in the way of meaningful domestic headline flow apparent. That leaves terminal policy rate pricing ~90bp or so above current levels, after a moderation from recent CPI-inspired hawkish extremes (which peaked pricing a little more than 110bp of hikes vs. current levels).

- Just over 75bp of tightening is priced over the next 3 MPC decisions, with outside odds of a > 25bp hike observed over that timeframe.

- Looking ahead, U.S. NFP data will likely provide the most notable input ahead of the weekend, while next week’s domestic docket is limited, headlined by final services PMI data.

- We don’t see anything in the way of BoE speakers pencilled in over the immediate term (at least for now).

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Jun-23 | 4.724 | +29.6 |

| Aug-23 | 5.010 | +58.2 |

| Sep-23 | 5.205 | +77.7 |

| Nov-23 | 5.333 | +90.5 |

| Dec-23 | 5.350 | +92.2 |

| Feb-24 | 5.322 | +89.4 |

| Mar-24 | 5.258 | +83.0 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok