Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

UK SONIA futures ticked slightly lower Thursday, between 0.5-1.5 ticks in the whites through greens.

- The highlight of the session was BoE chief economist Pill who triggered a modest selloff in rates when perceived to have distanced himself from comments made Monday in which he said the conversation about cuts could start in the middle of next year. He didn't repeat those comments today, with the overarching message that the BOE still has a hiking bias - as MNI observed though, his message didn't really change greatly from previously.

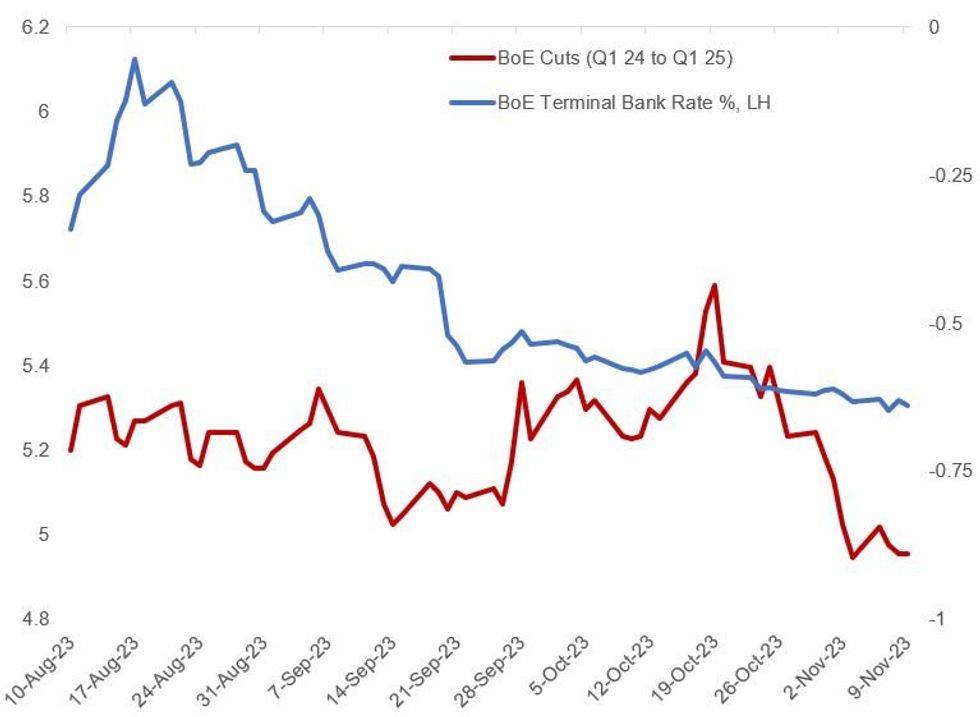

- Near-term expectations were little changed on the day, with around 4-5bp of hikes still priced for the rest of the cycle to a Feb 2024 peak; there's still around 90bp of cuts priced in the subsequent year.

- That said, for Mar24 through end-2024, there's 70bp of cuts seen - around 6bp more than priced before Pill spoke on Monday.

- Friday morning sees GDP / activity data first thing.

ECB rate pricing remained fairly steady through the session, with ECB speakers including Guindos and Villeroy not really moving the needle.

- With rates still seen unchanged through early next year, the first full 25bp cut remains priced by the June 2024 meeting. Total rate cuts of 90bp in 2024 remain priced.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok