Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

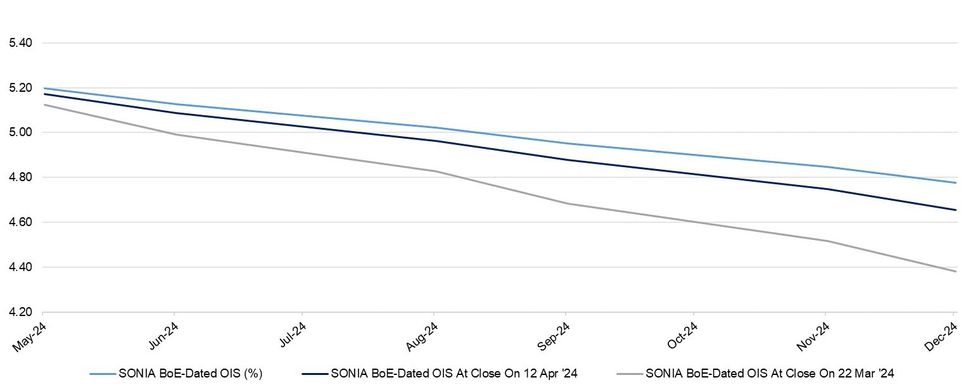

The last 4 weeks have seen ~40bp of ’24 BoE rate cut premium removed, leaving ~42bp of cuts priced through the Dec ’24 MPC.

- The combination of expectations for higher for longer U.S. rates and domestic data dynamics have driven the hawkish repricing.

- Last week’s hawkish offering from BoE’s Greene also factored in, although she has provided more balanced commentary in the time since.

- There was a brief showing below 35bp of ’24 cuts in the wake of Wednesday’s CPI data, although geopolitical angst and the relatively low degree of easing priced through year end factored into the recovery from this week’s extremes.

- This week's developments have also resulted in a raft of adjustments to sell-side BoE calls, most of which can be seen here.

- A summer rate cut remains on the table, although we concede that the recent data developments and global impulses have narrowed the path to that outcome.

- More progress is needed on the inflation and wage fronts for that to come to fruition, while geopolitical tensions provide a wildcard.

- Comments from BoE Deputy Governor Ramsden and former hawkish dissenter Mann are due later today (we will provide a preview of Ramsden’s address shortly).

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| May-24 | 5.198 | -0.0 |

| Jun-24 | 5.126 | -7.3 |

| Aug-24 | 5.023 | -17.6 |

| Sep-24 | 4.953 | -24.6 |

| Nov-24 | 4.848 | -35.1 |

| Dec-24 | 4.777 | -42.1 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok