Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

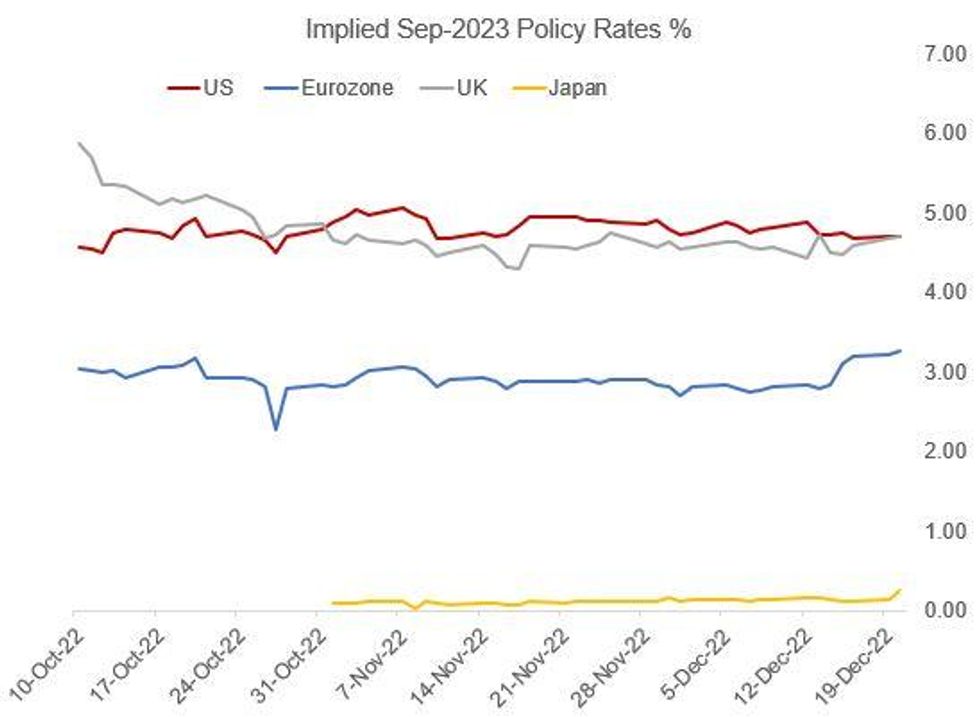

The BoJ's surprise shift in Yield Curve Control policy overnight has inevitably impacted Japanese rate hike expectations, and has had a modest spillover effect on global counterparts.

- The Japanese implied rate path had previously been basically flat through 2023, with modestly positive rates seen later in the year. Post-BoJ decision though, it implies a zero percent rates by April vs the current -0.10% target, with a full 20bp hike (the size of the BoJ's previous target rate move) by the July meeting.

- BoJ rate hike expectations still barely register on a comparison chart with the Fed/BoE/ECB, but the divergence with central bank counterparts in 2023 is now much less pronounced.

- Overnight, terminal ECB pricing has ticked 4-5 basis points higher to +138bp in hikes by Sept 2023 (3.38% depo rate)- BoE terminal pricing had implied another 134bp for Sept 2023, pulling back to currently (127bp in hikes from here, so 4.77% Bank Rate).

- US implied rates meanwhile are flat-to-lower. The Fed is seen peaking much earlier, in May 2023, at 4.87% (implying 55bp of further tightening), and a better-than-even chance by of a 25bp cut by September, with just under 50bp of cuts implied by year-end.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok