Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

The dovish move in rates may struggle to be reversed if Bostic's last comments are any indication. In his Nov 19th appearance he focused on inflation while downplaying wages as a "trailing indicator" adding he still wants to see positive real wage growth. Inflation measures have been supportive including today's prints on Manheim Used Car Prices & NY Fed inflation expectations (1yr at 3% vs. 3.4% prev.). Meanwhile wages was possibly the only component of Friday's labour data that could not be "explained away" unlike the below consensus UR (justified through decrease in participation rate driving strong fall in total employment) & increase in headline NFP (explained away by 2-month revisions that were larger). Wages on the other hand came in at 0.44% MoM vs. c0.3% - though fall in average weekly hours was used by some analysts as a dovish offset. Our US Eco's full review is out and his summary take was net hawkish report particularly in the face of a weaker ISM services employment.

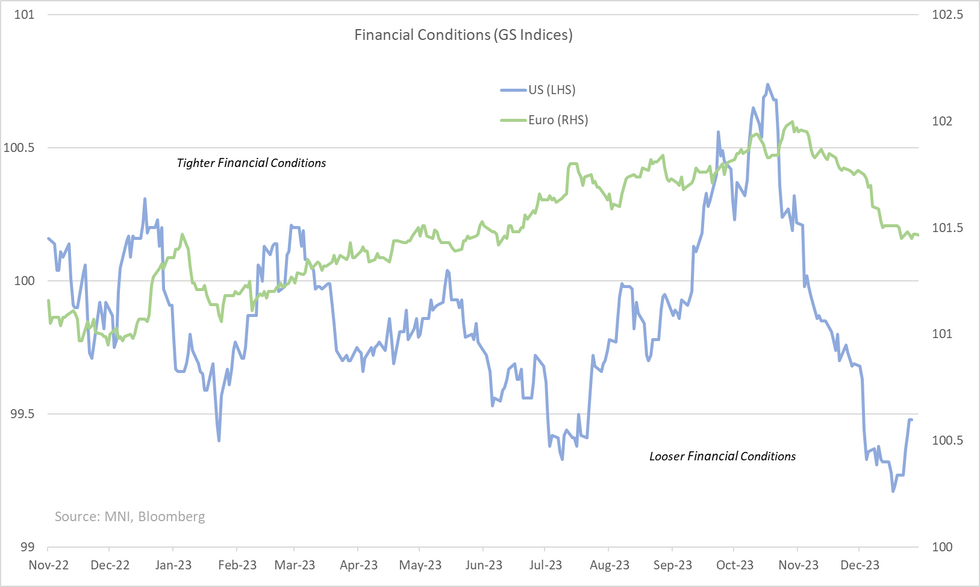

Re. financial conditions - something Fed speakers often are asked about but tend to downplay - we finally saw some recognition in the minutes; "Furthermore, participants observed that, after a sharp tightening since the summer, financial conditions had eased over the intermeeting period. Many participants remarked that an easing in financial conditions beyond what is appropriate could make it more difficult for the Committee to reach its inflation goal." We saw Dallas Fed's Logan ('25 Voter) reiterate this over the weekend. FI conditions have reversed since their Dec lows, partly due to rates (Fed pricing of cuts this yr are +15bps from lows) but also helped by equity & credit's sell-offs.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.