Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

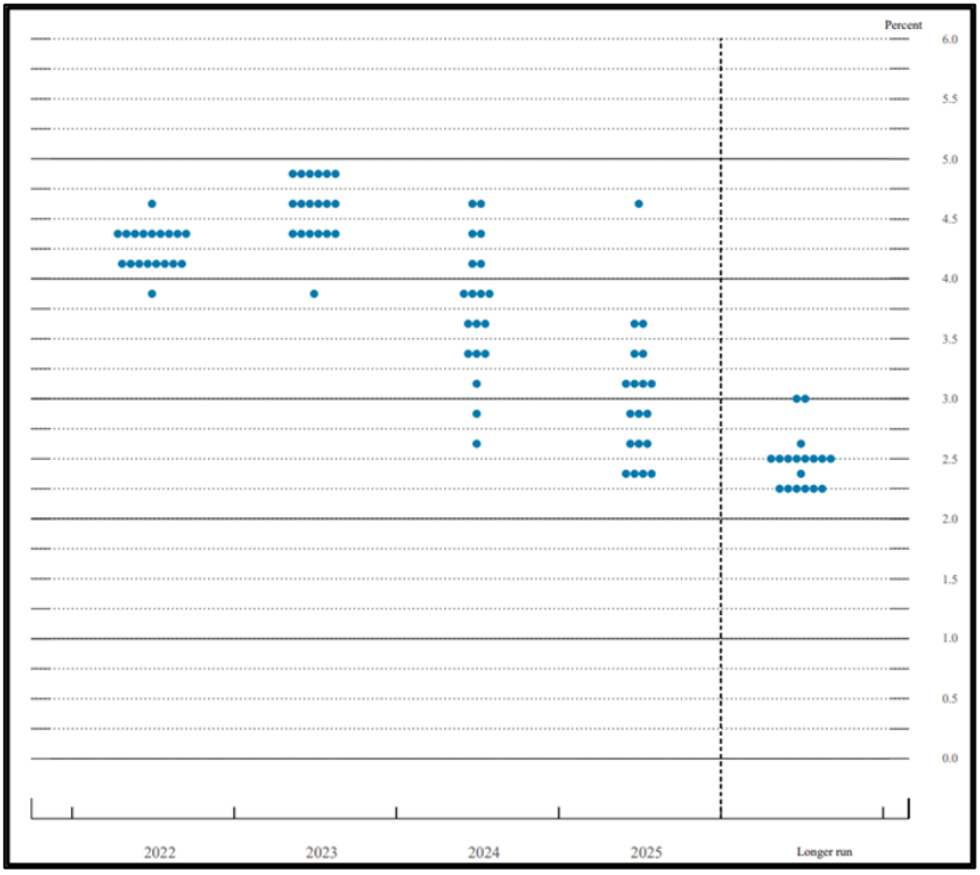

In what amounts to a modest pushback to market exuberance since last Thursday's CPI report by one of the more dovish members of late, Atlanta Fed Pres Bostic's essay published today makes clear more hikes will be needed. And like his FOMC colleagues, he doesn't seem convinced that much progress is being made on the inflation front.

- In early October he said he'd seen rates rising to between 4-4.5% by year-end before pausing. With a 75bp Nov hike in the interim, and rates at 3.75-4.00% now, that's consistent with him supporting a 50bp hike in December. But it now sounds like he wants to see further hikes in 2023 to get to a "sufficiently restrictive" level.

- A 4.6% dot for 2023 would be the minimum for his Dot Plot projection in that case, and more likely 4.9%. It's plausible he will remain toward the bottom end of projections (he was probably a 4.4% last time), which suggests the Dot Plot 2023 median will probably be upped from September's 4.6%. It could well augur a FOMC median dot above 5.00%.

- One other comment of note, as we try to pin down what Fed members consider to be the impact of lags: "A large body of research tells us it can take 18 months to two years or more for tighter monetary policy to materially affect inflation" but "there is considerable uncertainty about how these policy lags will play out."

- Note that taken literally, 18 months from the start of rate hikes in Mar '22 would be Sep '23, though a more generous interpretation is that the 18 months started in Oct '21 started signaling tighter policy ahead, meaning the lag would be felt by the end of Q1 '23.

Fed September SEP Dot PlotSource: Federal Reserve

Fed September SEP Dot PlotSource: Federal Reserve

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok