Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

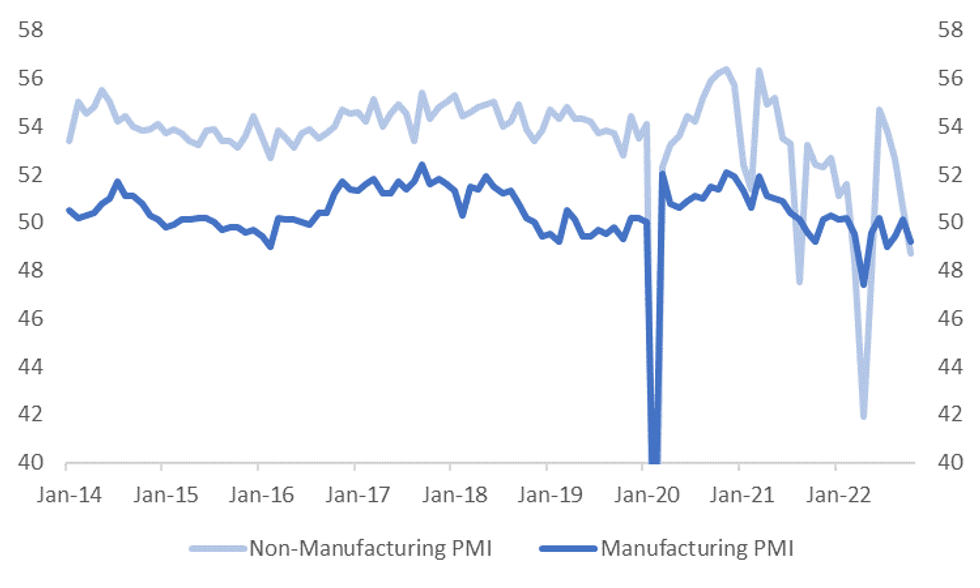

Both China PMIs were weaker than expected. The manufacturing print at 49.2, versus 49.8 expected and 50.1 previously. The non-manufacturing PMI fell to 48.7, against a 50.1 forecast and 50.6 prior. Interestingly, no economist surveyed pencilled in this degree of fall for the non-manufacturing PMI. The composite PMI fell to 49.0 from 50.9. These data prints point to downside risks for China growth momentum in the early stages of Q4.

Fig 1: China PMIs Both Into Contractionary Territory for October

Source: MNI - Market News/Bloomberg

- The manufacturing PMI headlines remains within recent monthly outcomes, but the non-manufacturing print is back to fresh lows since May of this year. It points to a decent loss of momentum for the services sector, given the headline reading was at 54.7 in June of this year.

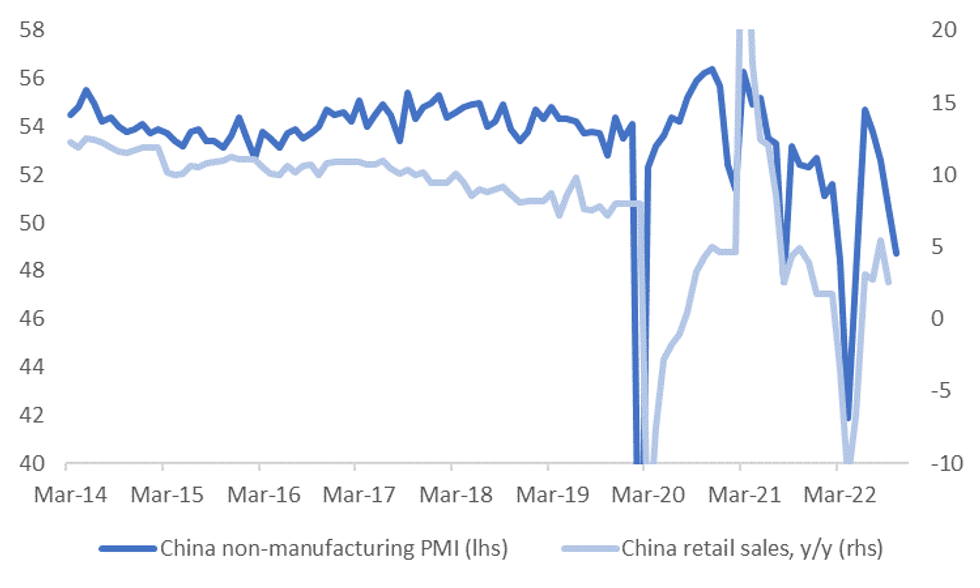

- This suggests further downside momentum in consumer spending indicators like retail sales, see the chart below.

- It also comes amid a more elevated backdrop for domestic covid case numbers as well as we head into November, which could inhibit any rebound in the near term.

- The detail of the PMI surveys showed disappointing outcomes for new orders (48.1 for manufacturing, fresh lows back to April, 42.8 for non-manufacturing) and employment also slipping against both survey readings. The only bright spot for the manufacturing PMI was a tick up in export orders to 47.6 (form 47.0).

Fig 2: China Retail Spending - Momentum Could Still Be Skewed To The Downside

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok