Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

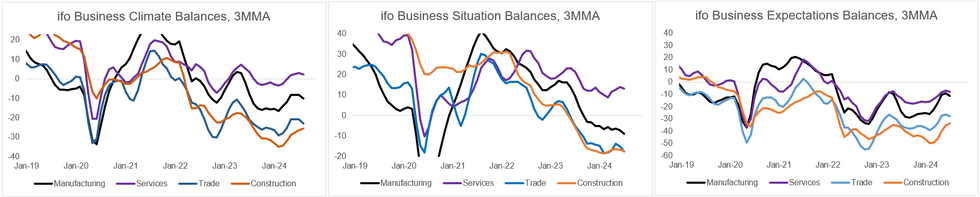

Germany's IFO Business Climate Index fell in July for the third consecutive time to 87.0, weaker than both expectations of 89.0 and June's 88.6. This is the lowest overall print since February, and mirrors the July flash PMIs, which also saw a decline in sentiment across sectors. The data reinforces the narrative of a stall of the gradual recovery in Germany, and the weaker business expectations in particular also lower expectations of that recovery going forward.

- Both main subindices fell: current assessment came in at 87.1 (vs 88.5 cons; 88.3 prior), and expectations underperformed even more, at 86.9 (vs 89.3 cons; 89.0 prior).

- The weakness was also broad-based across sectors: Diffusion balances fell everywhere. The decline in manufacturing to -14.1 (-9.3 June, back to Feb levels) was centered around businesses' current assessment (-13.9 vs -6.2 June, lowest since the pandemic), while services firms predominantly had worse expectations in July than before - keeping the overall services balance only barely in positive territory at +0.7 (vs +4.2 June, back to March levels; services expectations -11.1 July vs -5.2 June).

- In the trade sector, both the current assessment and expectations were weaker, the overall balance stands at -27.8 (-23.6 June). Construction, which saw the the lightest overall decline (but from already very low levels) to -26.0 (-25.2 June), the current assessment was worse (-18.7 vs -17.1), while expectations remained largely unchanged.

- The less volatile 3MMA measures mirror the underwhelming print: they fell for all sectors except construction, and clearly show that the uptrend towards the beginning of this year did not continue recently.

MNI, IFO

MNI, IFO

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok