Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CANADA DATA

Significant moderation on labor-related aspects:

- Wage growth expectations decline “significantly”, with labour costs seen increasing 3.4% over the next twelve months vs 4.1% in both Q1 and Q4. It’s the lowest since 1Q21 and close to the historical average of 3.2%.

- The share of firms reporting labour shortages as limiting ability to meet demand fell from 22% to 15%, its lowest since 2Q20 and below the 29% average since 2017.

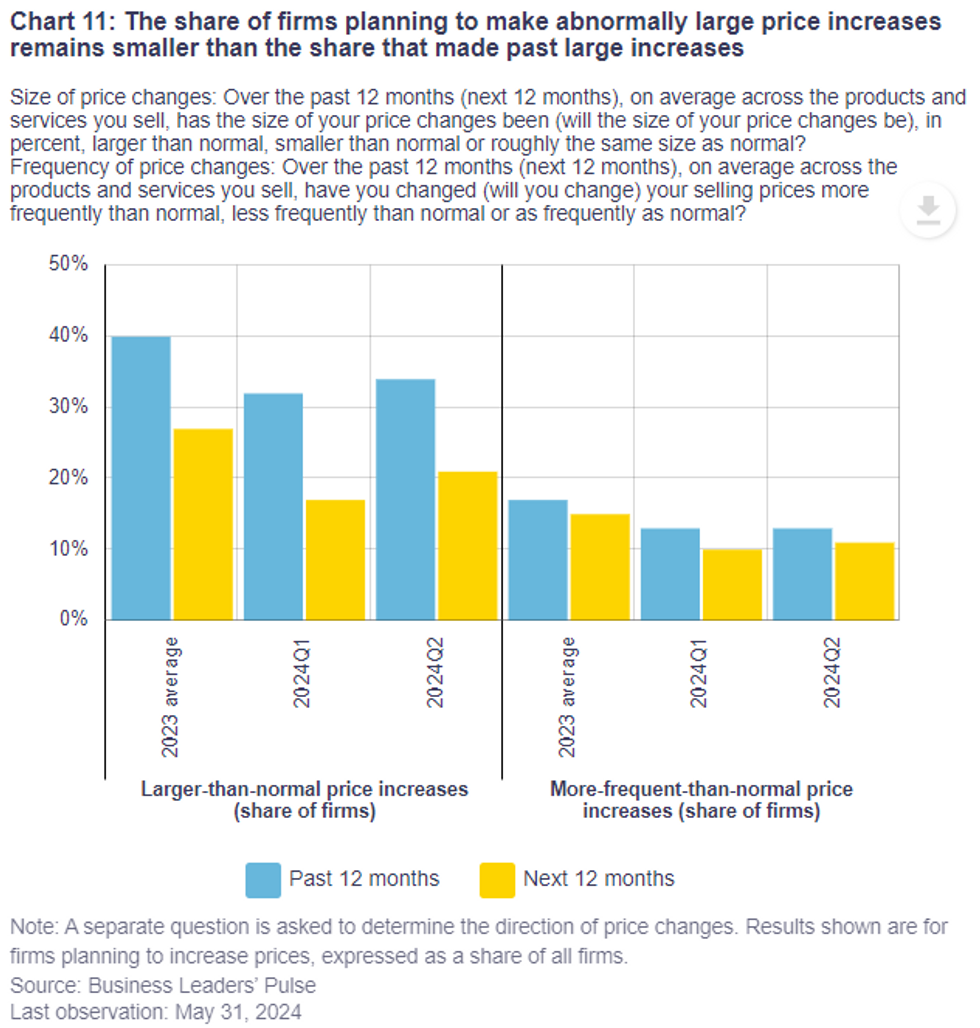

Price expectations see broad stalling in what had been good progress:

- The share expecting larger-than-normal price increases over the next twelve months increased from 17% to 21% in Q2 (vs the 27% average response to the same question in 2023).

- BoC commentary paints this in a positive light; it’s “well below” last year’s average and “considerably lower” than the 34% realized over the past year. However, the BoC make it very hard to know how this compares historically. Last quarter’s survey had a different question which showed 13% expecting output prices to increase significantly vs a pre-pandemic average of 11%.

- The increase in the share expecting larger than usual increases was at least partly offset by “more firms expect[ing] to keep prices flat”, whilst the share expecting more-frequent-than-normal price increases only marginally increased from 10% to 11% (averaged 15% in 2023).

- Inflation expectations generally flat over the quarter, with the 2Y unchanged at 3.0%. Monthly readings from the Business Leaders’ Pulse paint a similar picture.

- Fewer firms expect inflation of 2-3% over the next two years (from 54% to 48%). That more than offsets the 1pp increase for the share expecting inflation of >3% (from 40% to 41%) but a large increase in the no response share muddies the takeaway here.

Weak investment outlook:

- Investment intentions saw a tepid lift with a net 11% in Q2 expecting to increase investment spending on machinery & equipment over the next year after the 0% in Q1 was the lowest since 2Q20. It’s still below the 16% averaged since 2017.

Source: Bank of Canada

Source: Bank of Canada

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok