Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

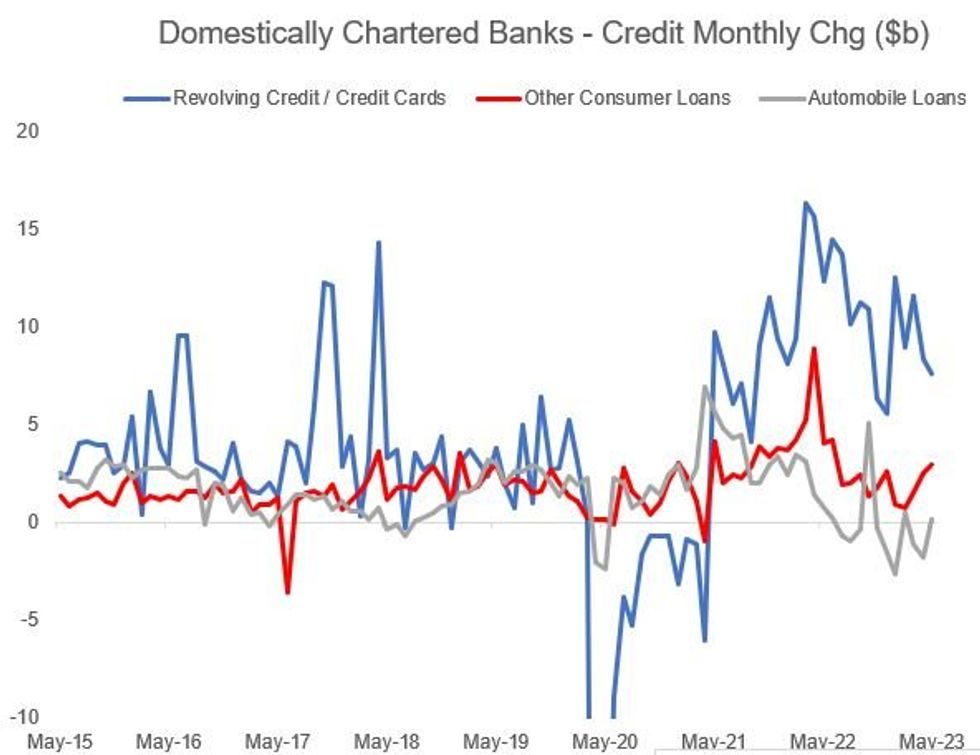

While there is continued evidence that consumer credit conditions are be tightening, including May's drop in nonrevolving lending, not all data points to a significant shift yet.

- The Fed's H.8 release (commercial bank assets and liabilities data) out last week for example shows that revolving credit growth for domestically chartered banks continues to grow at a near double-digit billion dollar clip monthly, rising since March's bank turmoil at a well-above pre-pandemic pace.

- While other consumer loans have flatlined, they haven't fallen sharply as of May. Automobile loans have struggled since late last year, while the remainder of the category (much of which is made up of student loans) has ticked higher.

- The latter is a little surprising given that loan repayments are due to restart imminently, but even with a reversion to zero growth, student lending hasn't been nearly as big a contributor to overall consumer lending from banks since late last year as have credit cards.

- Strong income growth and household balance sheets have been the main supports of US consumer activity anyway, and those haven't faded yet.

- While domestically chartered banks' consumer loans represent $1.9T, that's only 12% of their assets - and potentially more worrying are commercial and industrial loans ($2.3T) and real estate loans ($5.3T), of which commercial real estate ($2.8T) look especially troubled.

Source: Federal Reserve, MNI

Source: Federal Reserve, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok