Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EMERGING MARKETS

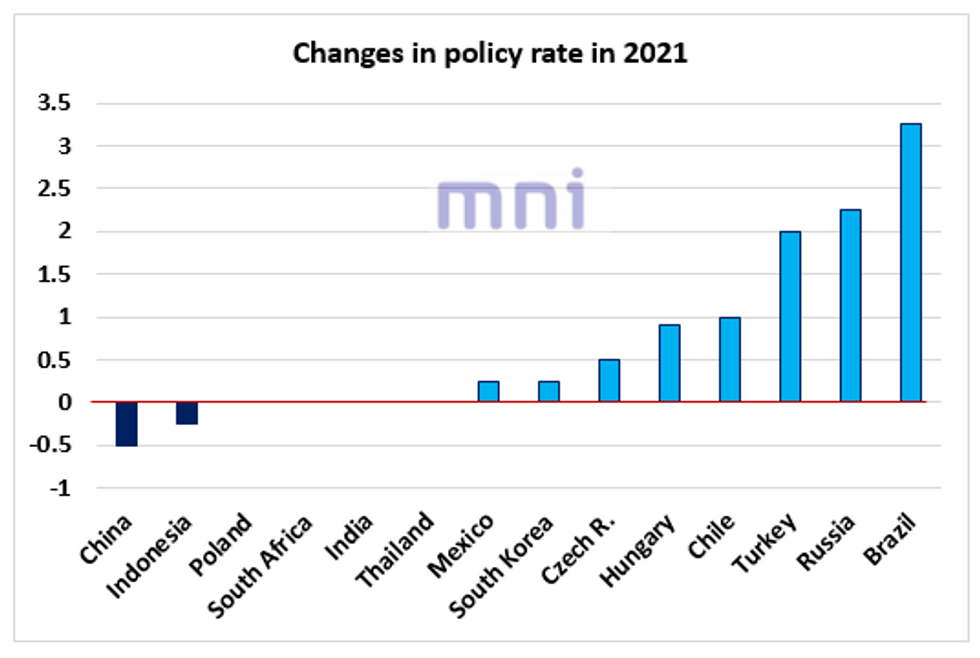

- As inflationary pressures remain firm in the EM world (especially Latam and CEEMEA), a rising number of central banks have embarked into a tightening cycle.

- Yesterday, Central Bank of Chile 'surprised' the market by taking a hawkish route, hiking by 75bps to 1.50% (vs. 50bps exp.) following a 25bps increase in July. The constant CLP weakness this summer amid elevated political uncertainty could also increase inflation risks in the coming months, therefore pushing the central bank to raise more 'aggressively'.

- Banxico also rose its policy rate by 25bps (a 'dovish' hike) in order to curb inflationary pressures, with CPI inflation coming in at 5.8% in July (vs. 4% CB upper tolerance band). Projections for headline inflation is expected to gradually decrease and converge towards the 3% target in Q1 2023.

- Brazil central bank raised the Selic rate by 100bps to 5.25% (unanimous decision) following three consecutive rate increases of 75bps, with the Copom expecting to deliver another 100bps hike at next meeting on Sep 21/22.

- In the CEE region, the NBH maintained a hawkish tone and raised the policy rate by 30bps (again) to 1.5% for the third consecutive time. HUF was the best performer among EM currencies in August, up 2.2% against the USD, strongly supporting Hungary equities (with BUX index trading close to its all-time high).

- Surprisingly, the NBP remains quiet despite headline inflation standing significantly above the 3.5% upper tolerance band (August CPI came in at 5.4% YoY). The majority of the NBP members is still aiming to keep interest rates low as the economic uncertainty remains elevated.

- Bank of Korea raised its policy rate by 25bps to 0.75% for the first time in nearly three years as financial economy has started to show some signs of overheating. The decision was not unanimous as the uncertainty over the economic recovery remains elevated.

- Interestingly, Asian and SE Asian currencies have performed strongly despite central banks keeping rate on hold due to the Delta variant; THB and INR were the second and third best-performing currencies in August, up 2% and 1.9% against the greenback, respectively.

- The rapid deceleration in inflation in Malaysia and Thailand in recent months combined with the broad ADXY strength in the past two weeks could be two explanations behind Asian and SE Asian currencies strength last month.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok