Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (London)

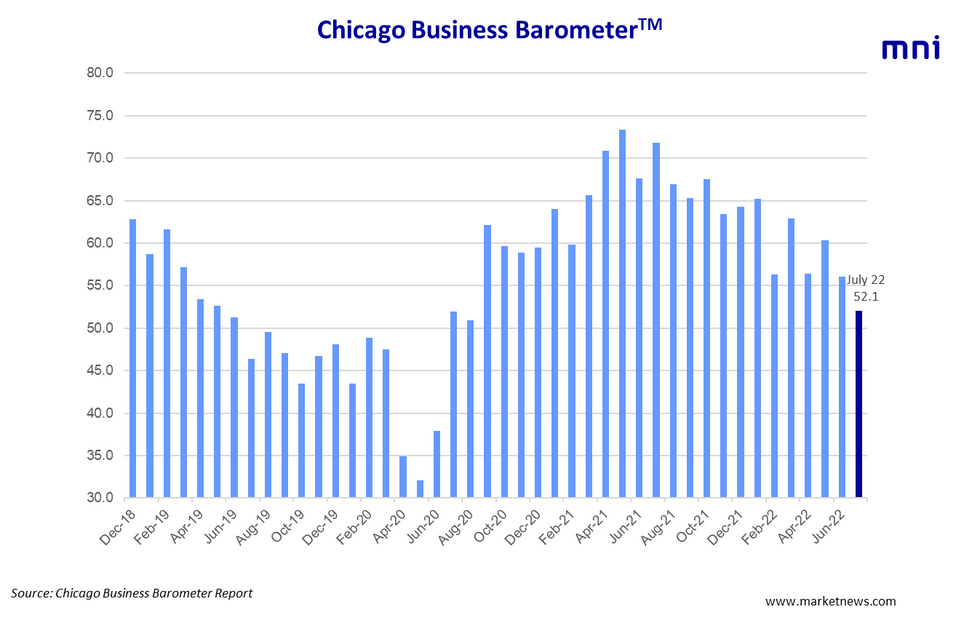

Key Points – July 2022 Report

The Chicago Business Barometer™, produced with MNI, slid further in July, extending June’s decline. The indicator fell 3.9-points to 52.1, the lowest level since August 2020.

- All main indicators decreased except for prices paid and employment, the latter of which hit the highest level since October 2021. Production, New Orders, Order Backlogs and Supplier Deliveries are all back around 2020 levels.

- Production fell 7.0 points to 48.2 in July, a two-year low. Close to a fifth of firms saw lower production.

- New Orders slid a further 5.4 points to 44.5, the lowest in 25 months. Overall demand waned in July.

- Order Backlogs slumped 6.8 points in July to 48.4. As new order levels softened, a quarter of businesses saw backlogs decline as they worked through postponed production.

- Employment grew 5.4 points to a current year high of 56.1 as the labor market continued to tighten.

- Supplier Deliveries ticked down 2.0 points to 67.1. This was the lowest since October 2020 as deliveries remained slow and lead times lengthened. Both the war in Ukraine and knock-on effects of Chinese lockdowns continued to hamper supply chains.

- Inventories saw the largest decrease this month, plunging 16.2 points. This is a stark difference to May’s near 50-year high.

- Prices Paid rose 2.3 points to 81.9 as price pressures intensified. Transparency issues regarding grounds for supplier price increases were flagged.

SPECIAL QUESTION

This month we asked firms “How are you looking to manage rising fuel prices affecting your running costs?”. Increasing charged prices was the mode tactic (56.7%), followed by 30% of firms reducing costs in other areas. Less businesses were reconsidering distribution plans (13.3%) and cutting back production (6.7%). 43.3% of firms were not intending to make changes or saw fuel prices not affecting running costs

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok