Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

(MNI Australia) A reminder that tomorrow delivers Q4 GDP in China, along with the Dec monthly run of activity figures. Expectations are fairly downbeat, not surprisingly, with Covid related headwinds prominent in the month.

- Q4 GDP is forecast at -1.1% q/q, range: -3.0%/+0.8%, prior 3.9%.

- IP is forecast at 0.2% y/y, range -3.7%/+3.7%, prior 2.2%

- Retail sales is forecast at -9.0% y/y, range -14%/0%, prior -5.9%.

- Fixed asset investment is expected at 5.0%, range 4.7%%/5.5%, prior 5.3%

- Property investment is forecast at -10.5%, range -17.5%/-9.5%, prior -9.8%.

- Jobless rate is expected at 5.8%, range 5.5/5.9%, prior 5.7%.

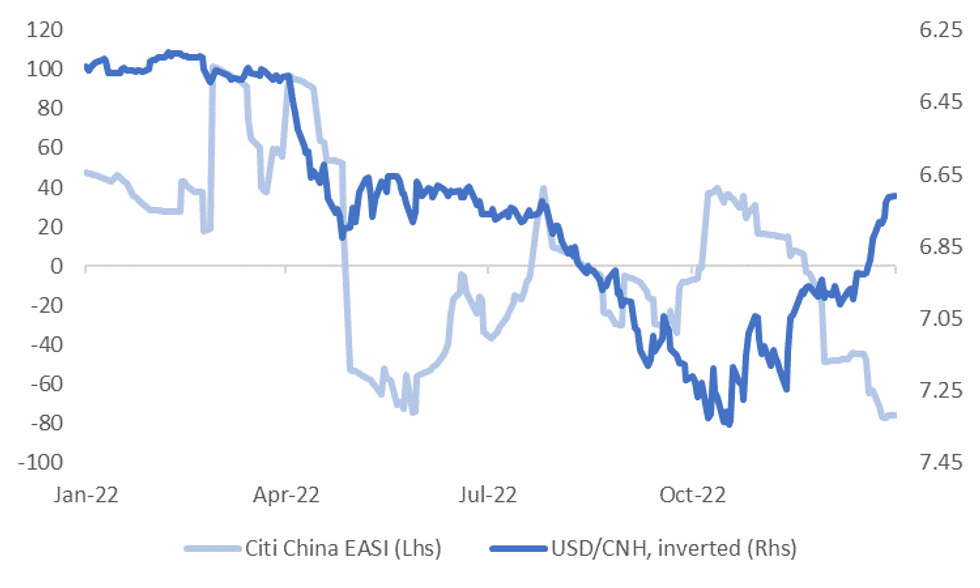

China related asset sentiment is largely shrugging off downbeat data outcomes since the exit from CZS. The chart below overlays the Citi China EASI against USD/CNH, which is inverted on the chart. We are around cyclical lows for the surprise index, but currency sentiment remains on the improve. As highlighted earlier, equity sentiment is also trending higher. So once again we may see limited fallout from the data, with market participants happy to look through softer outcomes and focus on the 2023 outlook.

Fig 1: Citi China EASI & USD/CNH (Inverted)

Source: Citi/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.