Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

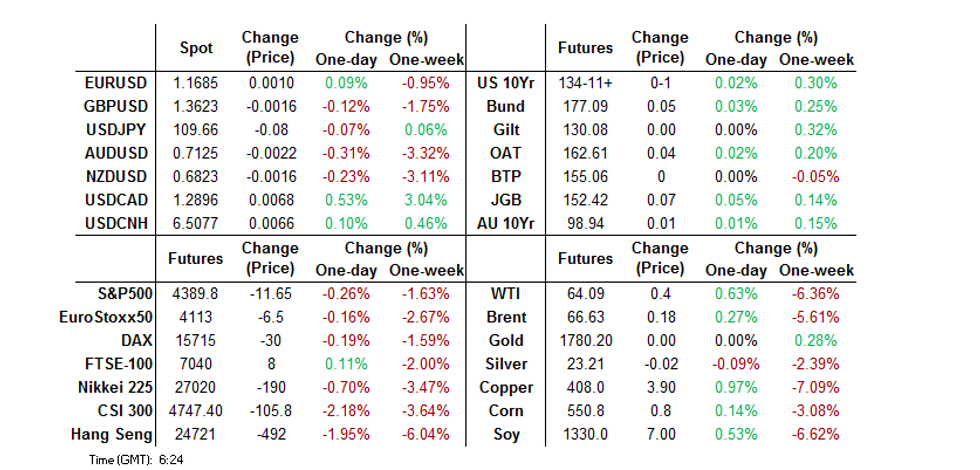

- The latest Chinese regulatory reach dampened sentiment in Asia.

- USD/CAD has punched above C$1.2900

- A limited docket rounds out the week.

BOND SUMMARY: Core FI Fails To Find A Spark On Friday

U.S. Tsy dealing was limited in Asia-Pac hours, with T-Notes operating in a 0-03 range, last 0-00+ at 134-11, while cash Tsys are little changed to ~1.0bp richer across the curve. Regulatory matters in China continue to provide the highlights on the headline front, and perhaps provided very modest support to the space. A ~30K lift of EDZ1/H2 was seen in Asia hours after heavy selling in the front end of the outright strip on Thursday.

- Another sedate Tokyo session for JGBs, with some peripheral headlines surrounding the local COVID situation, but nothing in the way of market-meaningful input. Futures +6, with the major cash JGB benchmarks little changed to 1.0bp richer out to 20s (5s outperform), while 30s and 40s are marginally cheaper on the day (longer dated swap spreads are a touch tighter as a result of the cheapening in JGBs). The monthly JSDA data pointed to trust banks buying a record net amount of super-long JGBs in July, while foreign investors lodged a record round of net buying of 10-Year JGBs in the same month.

- News that Sydney's lockdown has been extended through the end of September, with tighter restrictions imposed (including a curfew, compulsory mask wearing and limited exercise across some areas of the city) has had little impact on the space. YM +1.0, XM +0.5 after an early uptick faded. The latest round of ACGB Apr '25 supply saw a very strong cover of over 8.0x (note the DV01 & notional amount on offer was very limited), although the pricing wasn't particularly aggressive through prevailing mids (0.26bp) given the recent richening which has resulted in multi-month lows in yield terms. The space has been happy to look through the uptick in ACGB issuance size scheduled for next week, although the $2.0bn of ACGBs on offer during the week isn't anything like the regular amounts we saw tendered in the recent past (it will of course be supplemented by the previously outlined round of indexed bond issuance via syndication).

FOREX: CAD Sustains Further Losses; Antipodean Pairs Pressured By Lockdowns

Sentiment remained broadly negative in Asia, the greenback continued its move higher early in the session but has retreated as the session wears on, brining major pairs back towards neutral levels heading into Europe.

- AUD/USD is down 6 pips, but well off worst levels. The Sydney lockdown was extended until the end of September, there were 642 new coronavirus cases reported, down from a record 681 yesterday.

- NZD/USD is down 4 pips having recovered from session lows. In New Zealand the countrywide lockdown was extended to midnight on 24 August; there were 3 case discovered in Wellington, the outbreak had previously been contained to Auckland. New Zealand PM Ardern said the country was in a "reasonable position" on the outbreak.

- USD/JPY is up 9 pips. Data showed CPI fell less than expected in July, dropping 0.3% against a consensus of a 0.4% decline. Core-Core CPI fell 0.6% against an estimated decline of 0.8%.

- USD/CNH rose 58 pips, the PBOC kept LPR rates on hold – there was an outside chance of a cut after some of the recent dovish PBOC moves, but state media telegraphed that the PBOC is unlikely to cut LPR rates in August.

- USD/CAD continued to March higher, topping C$1.2900 despite little in terms of idiosyncratic headline flow and slight bounce in oil.

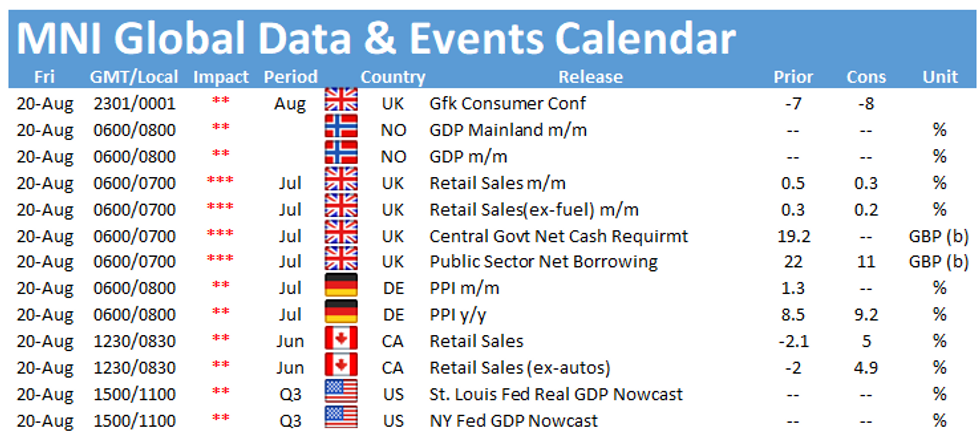

- Elsewhere UK GfK consumer confidence printed -8 in August compared to -7 expected, GBP/USD is down 9 pips while EUR/USD is up 9 pips.

- Looking ahead markets await German PPI data and US retail sales figures.

FOREX OPTIONS: Expiries for Aug20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1675(E506mln), $1.1700(E831mln), $1.1800(E737mln)

- USD/JPY: Y106.80($1bln), Y108.70-75($1.1bln), Y110.00-20($880mln)

- AUD/USD: $0.7425(A$750mln)

- USD/CAD: C$1.2575-85($630mln), C$1.2600($693mln), C$1.2700($570mln)

- USD/CNY: Cny6.4700($1.4bln)

ASIA FX: KRW Swings From Gains To Loss

An up and down session with the greenback tempering early gains, most Asia EM currencies starting positive, turning negative and now head into the close flat/with minor gains.

- CNH: Offshore yuan is stronger, the PBOC kept LPR rates on hold – there was an outside chance of a cut after some of the recent dovish PBOC moves, but state media telegraphed that the PBOC is unlikely to cut LPR rates in August.

- SGD: Singapore dollar gained, rising from the lowest levels in a month. Officials said late yesterday that Singapore will trial quarantine-free travel lanes for vaccinated passengers next month from Germany and Brunei as well as opening up to visitors from Hong Kong and Macau.

- TWD: Taiwan dollar is weaker, USD/TWD approaching the 28.00 handle. Markets look ahead to BOP current account data today, export orders are expected to have risen 21.2% in July

- KRW: Won is weaker, giving back early gains as USD/KRW hit the highest levels since September. South Korea extend current social distancing restrictions for two weeks

- MYR: Ringgit gained, Ismail Sabri has the support of 50 MPs and temporary PM Muhyiddin Yassin has also endorsed his former deputy.

- IDR: Rupiah is weaker and the worst performer in Asia. Indonesia's current account deficit widened to 0.8% of GDP in Q2, balance of payments deficit was $0.4b in Q2, from $4.1b of surplus in Q1.

- THB: Baht is flat, in a consolidation pattern ahead of a vote on the second and third readings of the fiscal 2022 budget.

- PHP: Peso gained, halting a two-day decline. Metro Manila region will downgrade to the second-strictest movement restrictions from Aug. 21 to Aug. 31.

ASIA RATES: Early Moves Reversed

- INDIA: Indian markets will return from a holiday today to a wave of activity in the form of RBI minutes and an INR 260bn auction. Markets will look to the minutes for confirmation of the dovish bias and any further clues of bond market support. The latest RBI bulletin showed the Central Bank is focused on supporting economic growth and will look through supply side inflationary pressures. In terms of the auctions the sale will feature the benchmark 10-Year bond. The RBI will today sell INR 260bn consisting of INR 30bn 4.26% 2023 bonds, INR 140bn 6.1% 2031 bonds and INR 90bn 6.76% 2061 bonds.

- SOUTH KOREA: Futures reversed early losses and posted small gains. Markets continue to focus on coronavirus developments which saw social distancing measures extended for two weeks, though restrictions for private gatherings of four people are allowed as long as there are two vaccinated members in the party. South Korea said that 48.3% of the population have had the first vaccine, while 21.6% have been fully vaccinated.

- CHINA: Futures in China lower, even as equity markets drop. 10-Year future down 6.5 ticks. the PBOC kept LPR rates on hold – there was an outside chance of a cut after some of the recent dovish PBOC moves, but state media telegraphed that the PBOC is unlikely to cut LPR rates in August. The PBOC matched maturities with injections, repo rates slightly higher but respecting recent ranges. Evergrande's bonds are under pressure but off worst levels, the firm said it would address its debt issues after the CBIRC issued a public reproach.

- INDONESIA: Yields higher in Indonesia, some curve flattening. Indonesia will offer a retail sukuk from Aug. 20 to Sept. 15, with a fixed return rate of 5.1%. Funds from the sale will be used to finance the state budget. The Bank Indonesia left rates unchanged yesterday and said it had a plan to address tightening from the US when it came.

EQUITIES: Another Broadly Negative Session In Asia

Equity markets in the Asia-Pac time zone ended the week with another broadly negative session, sentiment remains negative as markets contemplate the spread of the delta variant of coronavirus and China's regulatory crackdown. Markets in mainland China led the way lower, the CSI 300 down over 2%, ChiNext declined by over 3.0%, the most since July 27. The healthcare/medical sector is the latest in the crosshairs of China's regulatory watchdogs while Evergrande was also told to resolve its debt problems which added to negative sentiment. Markets in Japan are lower to the tune of around 1.0%, some peripheral headlines surrounding the local COVID situation, but nothing in the way market-meaningful input, CPI fell slightly less than expected. Markets in New Zealand also lower after coronavirus cases were discovered in Wellington, the outbreak had previously been confined to Auckland. In the US futures were lower after a mixed finish on Thursday.

GOLD: In The Recent Range

Participants have showed a lack of conviction over the last 24 hours or so, allowing spot gold to operate within the confines of the recently observed range, last dealing ~+$5/oz at ~$1,785/oz. A reminder that the USD (broader DXY) has printed fresh multi-month highs over the last 24 hours, while our weighted U.S. real yield indicator has consolidated in the upper end of the range witnessed since mid-July. Next week's annual Jackson Hole Symposium, hosted by the Kansas City Fed, presents the next key macro event risk for bullion. Participants will eye any discussions surrounding the tapering topic, with Fed Chair Powell's address set to headline.

OIL: On Track For Weekly Loss

WTI is up $0,40 vs. settlement, with Brent ~$0.20 better off, Both benchmarks on track to finish with losses of around 6.5%. The WTI benchmark is now over 18% off the July highs, meaning further weakness could tip oil into bear market territory. WTI has support at $63.17 - 1.00 proj of the Jul 6 - 20 - 30 price swing while resistance is seen at $67.48 - High Aug 13, Brent has support at $63.89 - Low May 21, while resistance is seen at, $65.75 - Low May 24 support turned resistance.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.