Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CNH

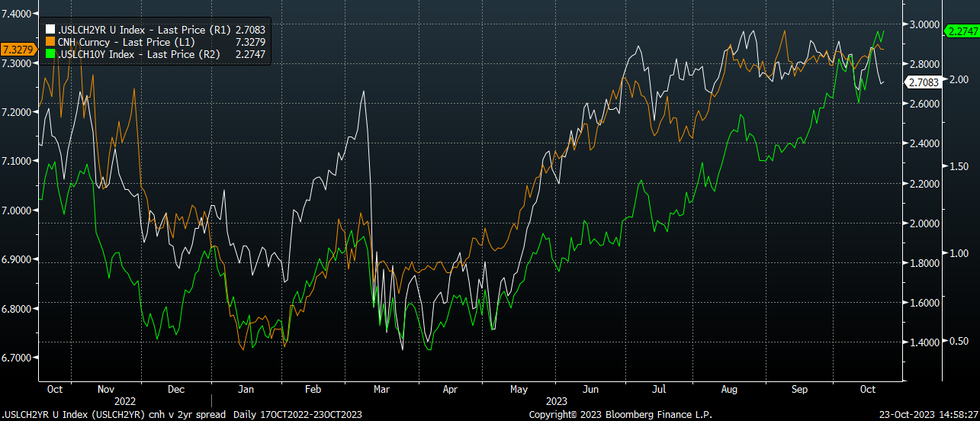

USD/CNH has had a relatively quiet start to the week. The pair tracking recent ranges and last near 7.3280, little changed versus closing levels at the end of last week. Local equities continue to weaken, although as we noted earlier, this perhaps less of a headwind for the local FX given equity losses elsewhere in terms of the major indices. The China to rest of the world equity trend only sits down slightly.

- In terms of rate differentials with the US, we have diverged somewhat recently. The US-CH 2yr government bond yield spread is down from recent highs back to +270bps, but the 10yr spread has continued to track higher, last at +228bps.

- This largely reflects gyrations in terms of the US Tsy yield curve, with the recent steepening trend dominating. Still, the China 2yr yield has recovered from earlier 2023 lows, last near 2.42% (back in August lows were around 2.07%).

- USD/CNH hasn't followed the 2yr spread lower (white line on the chart below), see the chart below. In the past 3 months the correlation between USD/CNH and the 10yr spread (green line on the chart), has been stronger though at +69%, versus +36% for the CNH and the 2yr spread with the US.

Fig 1: USD/CNH & 2yr US-CH & US-CH 10yr Spread

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok