Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

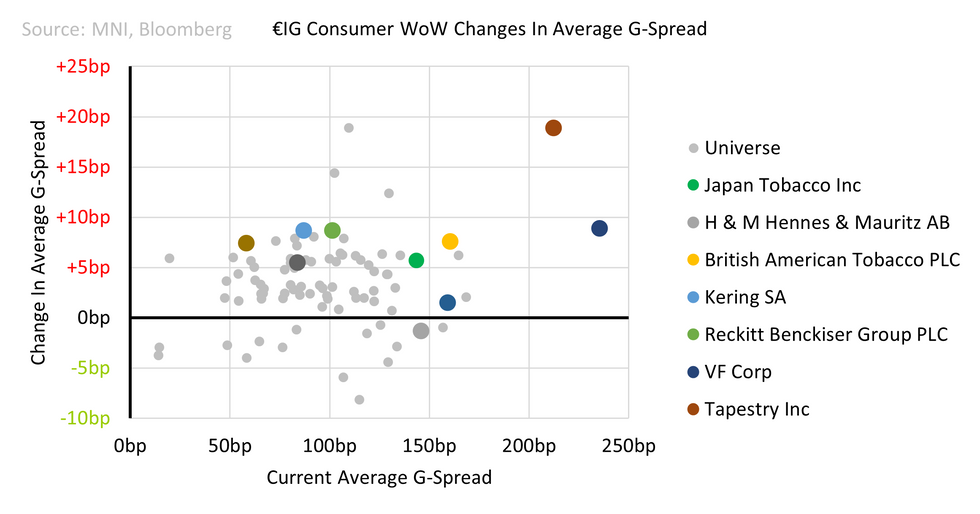

Key data points were skewed to positive; strong beat on US March nominal retail sales, LVMH 1Q firmer than Kering's 1Q guidance on luxury retail conditions & Adidas with a strong beat. Only point of disappointment was UK (real) retail sales this morning - less weighting for us on this though.

FTC headlines on Tapestry acquisition of Capri finally generated vol for bonds - we saw clear opportunities earlier but this weeks moves leave bonds at fairer levels now. Tapestry moves have given VF some company who continues to trade well wide of IG - we don't see earnings coming up showing a turnaround on headline numbers, hence cautious on VF for now.

We did flag BBB tobacco tends to underperform on spread-sell off's and we did see that this week. It's left BAT with a rough 2-weeks after it short-end/belly struggled on pricing last week.

LVMH earnings; https://marketnews.com/lvmh-aa3-aa-s-mc-fp-equity-...

Kering downgrade to A- Stable; https://marketnews.com/kering-nr-a-stable-ker-fp-e...

Tapestry latest; https://marketnews.com/tapestry-tpr-baa2-bbb-doubl...

VFC earnings coming up; https://marketnews.com/vf-corp-vfc-baa3-neg-bbb-ne...

Adidas earnings; https://marketnews.com/adidas-a3-a-double-neg-ads-...

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.