Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CROSS ASSET

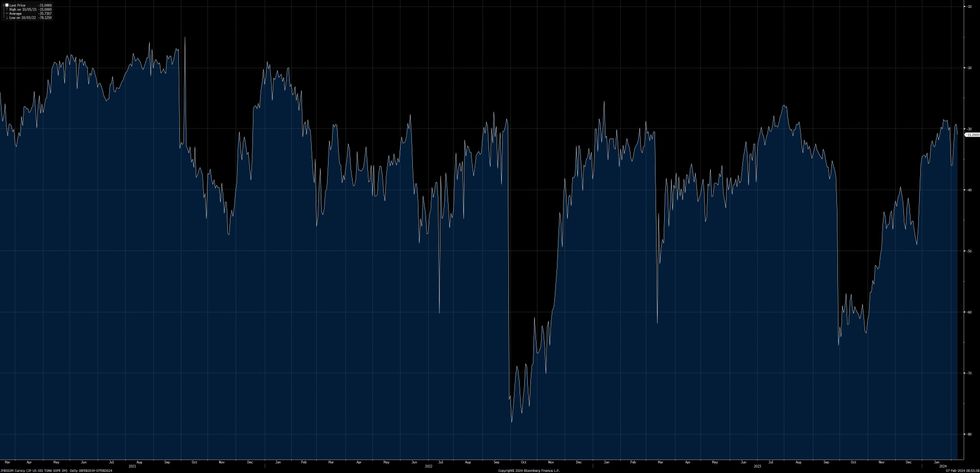

USD funding matters got some attention in Asia. We flagged the spill over into x-ccy basis in the wake of the initial round of NYC Bancorp worry (as footprints of USD demand showed up via those channels). That move evaporated (in 3-month tenors), but a fresh, albeit shallow, downtick in JPY/USD 3-month x-ccy basis has been seen, pointing to some potential worry on that front out of Tokyo.

- A large block buy (+20K) in SFRH4 futures was also seen in Asia-Pac hours, which could point to further USD funding-related worry in the region given that 20K SOFR blocks are a very rare sight in that timezone.

- A reminder that Japanese lender Aozora Bank has fallen afoul of its U.S. CRE exposure, with the company’s Tokyo equity listing losing over 30% in recent sessions. Japanese Finance Minister Suzuki has attempted to placate any worry re: overall Japanese exposure to those issues, stressing that lending to the U.S. real estate market is limited when you look at the totality/size of the Japanese banking sector.

- Pockets of U.S. CRE-related worry have also shown up in European financial names with related exposure in recent sessions.

- Once again, ee highlight that the moves seen in major USD x-ccy measures were limited last week and quickly unwound.

- The moves were also very shallow when compared to swings seen during the initial COVID outbreak and during last year’s U.S. regional banking sector malaise.

- They were also limited when compared to most instances of year end-related (turn) USD demand.

- We have suggested on several occasions that the headwinds faced by NYC Bancorp do not seem to be systemic in isolation, although worry re: U.S. CRE exposure will continue to provide a point of interest owing to the post-COVID evolution of home-office work splits.

- NYC Bancorp saw Moody’s downgrade the name to junk status after hours on Tuesday.

- The U.S. regional banking index KBW has shed a little under 5% vs. late January closing highs, with the index failing to get anywhere totally recouping the ’23 downturn.

Fig. 1: JPY/USD 3-Month X-Ccy Basis

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok