Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

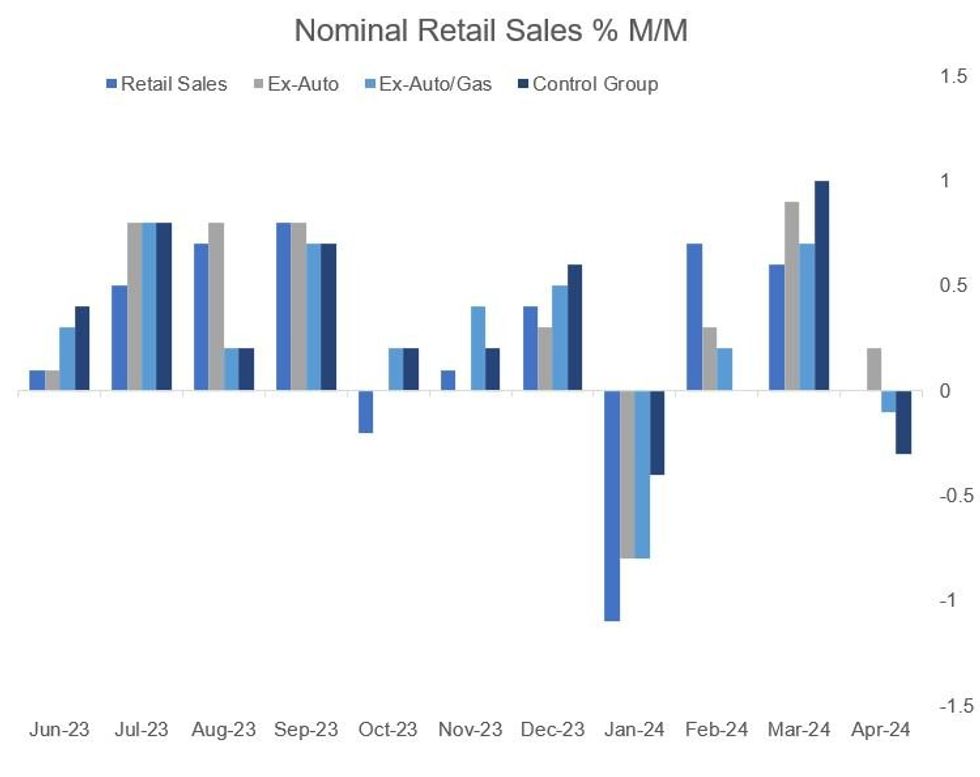

US retail sales had their poorest performance in 3 months in April, with weakness evident across the board, partially reversing March's strong gains.

- Overall retail sales were flat (+0.4% expected), pulling back from +0.6% in March, while ex-auto/gas sales were -0.1% (+0.2% expected) vs +0.7% in March. Each represented the poorest outturn in 3 months.

- The "control group" contracted by 0.3% M/M (+0.1% expected, and after +1.0% in March), the 3rd flat/negative reading in the past 4 months.

- The prior (March) figures also incorporate downward revisions across all major subcategories.

- Looking at individual business categories, motor vehicle/parts dealers were the biggest negative standout at -0.8% M/M, with sales in several other retail categories also negative including furniture, health/personal care, sporting goods, general merchandise stores, and nonstore retailers.

- Electronics and appliance stores (+1.5%), clothing (+1.6%) and and gasoline stations (+3.1%) were standouts on the upside, the latter largely due to higher gas prices.

- In real (CPI deflated) terms, retail sales fell by 0.3% Y/Y after a slight positive Y/Y reading in March - bigger picture, this series has basically been flat since 2Q 2021.

- The volatility in the retail sales series makes it difficult to draw too many conclusions on the health of the consumer with a single month's reading, but the reasonably broad-based softness and the contraction in the GDP-input control group suggest some moderate cause for concern as 2Q 2024 gets underway.

Source: Census Bureau, MNI

Source: Census Bureau, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok