Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

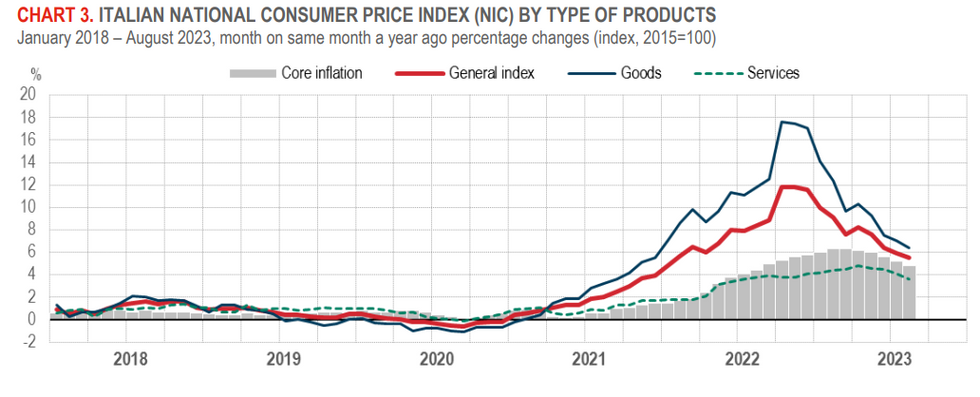

Italy's flash August HICP and CPI NIC both printed at 5.5% Y/Y, below the July prints of 6.3% Y/Y for HICP and 5.9% for CPI NIC. Overall, the reading came one the soft side of expectations, with the step-down in core inflation the key focus. Indeed Italy's figures helped keep the Eurozone aggregate M/M core reading from printing an unrounded 0.4% M/M (it came out at 0.34%).

- Core HICP (ex-energy, alcohol and tobacco) was 4.1% Y/Y (vs 4.7% prior) and flat on the month following a -2.0% M/M fall in July.

- Monthly HICP printed at 0.2% M/M (vs -1.6% prior) while CPI NIC was 0.4% (vs 0.0% prior). The larger fall in HICP compared to NIC was due to summer sales, which are only considered by the former measure.

- Food, alcohol and tobacco HICP prices rose 9.3% Y/Y (vs 9.8% in July). On a sequential M/M basis, unprocessed food saw a second consecutive deflationary print in August, with HICP inflation of -0.5% (vs -0.8% prior).

- Energy HICP inflation was 1.8% M/M (vs -1.4% prior), ending an 8 month streak of sequential monthly deflation (-0.1% Y/Y vs +0.6% Jul).

- Looking at core: non-energy industrial goods were -0.5% on the month, a step up from the -5.2% July print; Y/Y the deceleration was sharp though at 4.4% vs 5.2% in July. Clothing/footwear prices pulled back sharply, -3.1% M/M and to +2.8% Y/Y vs 5.4% in July, which may reflect the base effect of a shift in sales periods.

- Services disinflation was likewise key to the core disinflation, with Y/Y at 4.0% vs 4.6% in July. It was the 2nd consecutive 0.3% M/M outturn and well below rates 2x / 3x that magnitude earlier in the summer. Larger HICP services categories including restaurants/hotels and recreation decelerated Y/Y.

Source: Istat

Source: Istat

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok