Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

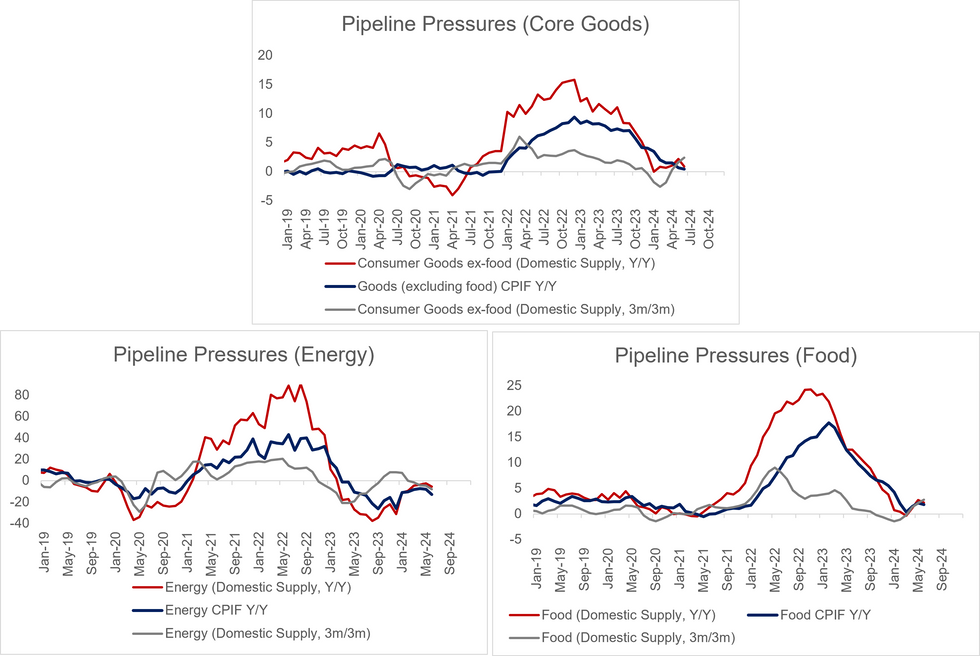

Swedish PPI fell 0.4% M/M in June, with energy base effects helping pull the annual rate down to 0.8% Y/Y (vs 2.6% prior). The price index for domestic supply saw similar dynamics, falling 0.4% M/M and rising 1.0% Y/Y (vs 2.6% prior).

- On a 3m/3m basis, the price index for domestic supply rose 0.8% (vs 0.9% prior), although the index excluding energy rose 2.7% (vs 2.1% prior).

- This acceleration reflected an increase in the 3m/3m rates of capital goods (1.7% vs 1.4% prior), consumer goods ex-food (2.4% vs 1.6% prior) and food (2.8% vs 2.2% prior).

- The pipeline prices suggest core goods CPIF disinflation should stall in the coming months. In June, goods CPIF inflation was -0.7% M/M and 0.4% Y/Y (0.6% in May).

- The domestic supply index combines domestic producer prices and imported prices, thus is a better gauge of CPI pipeline pressures.

- Elsewhere, lending from monetary financial institutions to households rose 0.7% in June (vs 0.7% prior), while deposit and lending continued to ease (in line with Riksbank signalling for further monetary easing in 2024).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok