Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

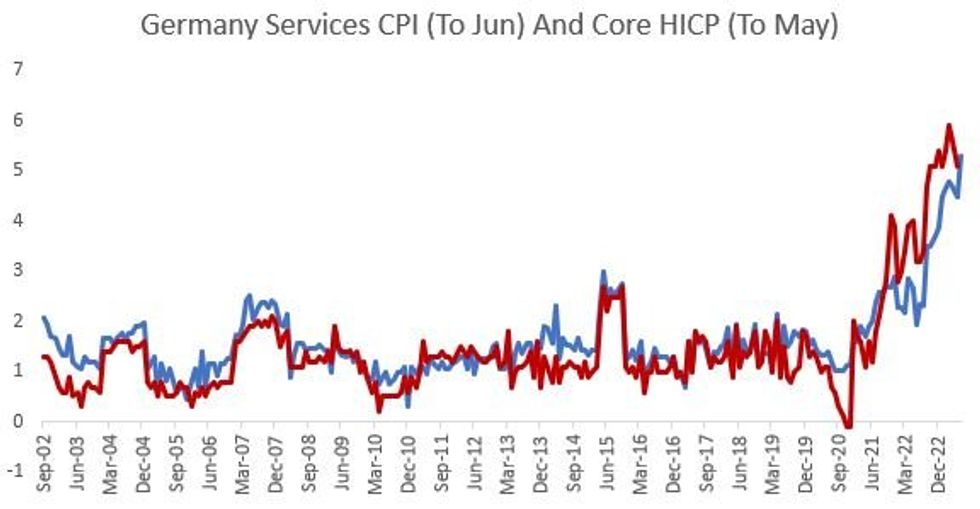

Tracking Eurozone core (coming into this week had been expected to tick up to 5.5% Y/Y vs 5.3%) is more difficult to ascertain given a lack of core HICP (as opposed to CPI) prints.

- But the German core CPI Y/Y acceleration (+5.8% from +5.4%, effectively reversing May's 0.4pp drop from April) was the most important and had been well anticipated as the major factor behind the overall expected Eurozone acceleration.

- The German report today showed services notably accelerating to a fresh post-1994 high (+5.3% Y/Y from 4.5% in May) and more than offsetting softer goods prices (7.3% after 7.7%). Though there's no detailed breakdown available, Destatis confirmed that it was the base effects from last year's introduction of the 9 euro transport ticket that was responsible, with state-level prices showing related transportation costs up more than 100% Y/Y vs Jun 2022.

- Elsewhere, Spanish core CPI surprised to the upside (+5.9% vs 5.5% survey) but ticked lower vs May at 5.9% from 5.1%, while core HICP in Italy pulled back to 6.0% from 6.4% prior. Combined those two have equal weighting to Germany, so the 0.2pp EZ pickup in core Y/Y HICP expected in June looks to remain in play.

- Following the German data, Goldman Sachs stuck to its expectation for an upside surprise and left its core expectation estimate unchanged at 5.56%, having entered inflation week at 5.61%.

Source: Eurostat, Destatis, MNI

Source: Eurostat, Destatis, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok