Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

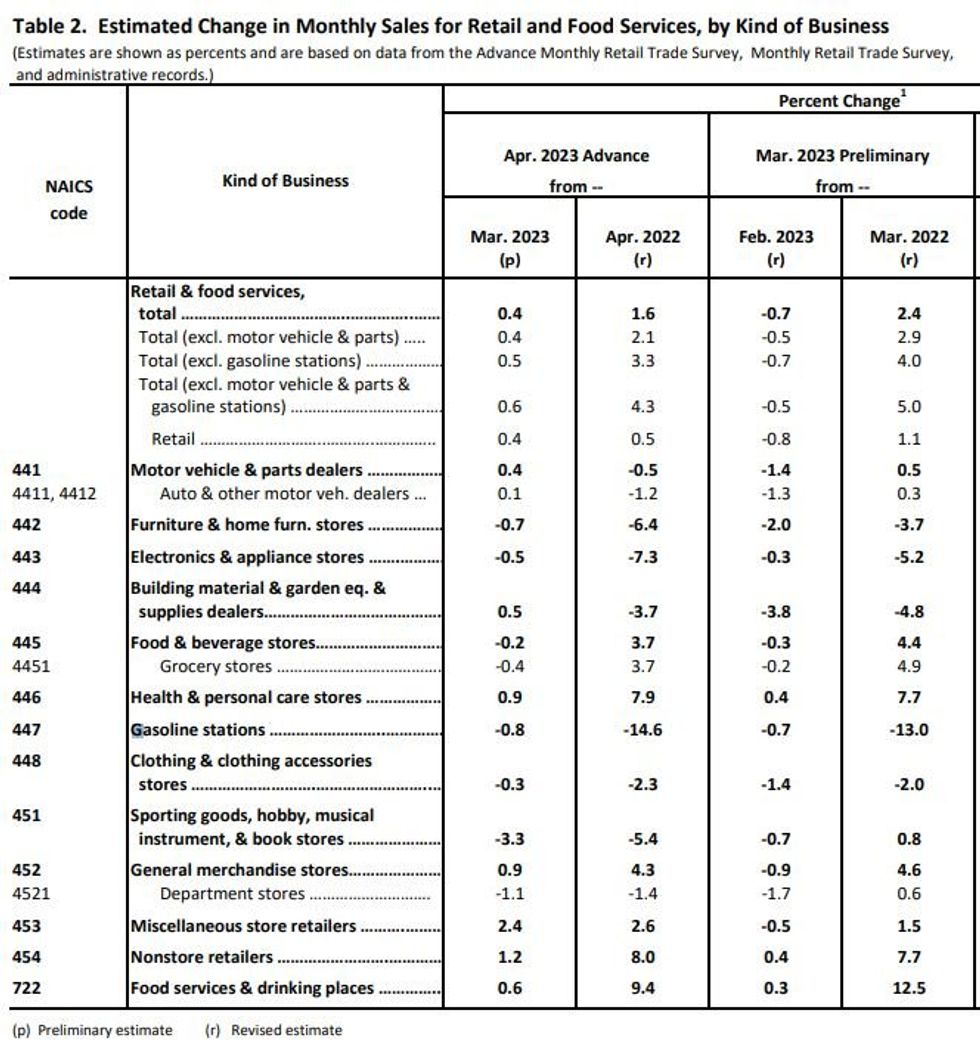

US April retail sales came in below consensus on the headline figure (+0.4% M/M vs 0.8% expected) and was in-line on ex-autos (+0.4% vs +0.4% exp.), but there were upward revisions to March for both (respectively by 0.3pp to -0.7%, and by 0.3pp to -0.5%).

- Conversely, the more "core" categories were stronger than expected, but saw March downgraded: ex-auto and gas grew +0.6% M/M (vs +0.2% exp; March lowered 0.2pp to -0.5%), while the GDP-input control group was +0.7% M/M (vs +0.4% exp, March lowerd 0.1pp to -0.4%).

- Details by category were mixed: in the biggest 5 categories, motor vehicles strengthened, as did general and nonstore retailers; weaker were food/beverage, and food services/drinking places.

- The strength in the core readings, especially the congrol group, presents a better-than-expected picture of US consumption in April.

- But the broader picture suggests nominal retail sales continue to flatline (+2.4% Y/Y growth), and remain below the Jan 2023 peak. That's not entirely surprising given the ongoing shift toward services and away from goods consumption.

Source: US Census Bureau

Source: US Census Bureau

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok