Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

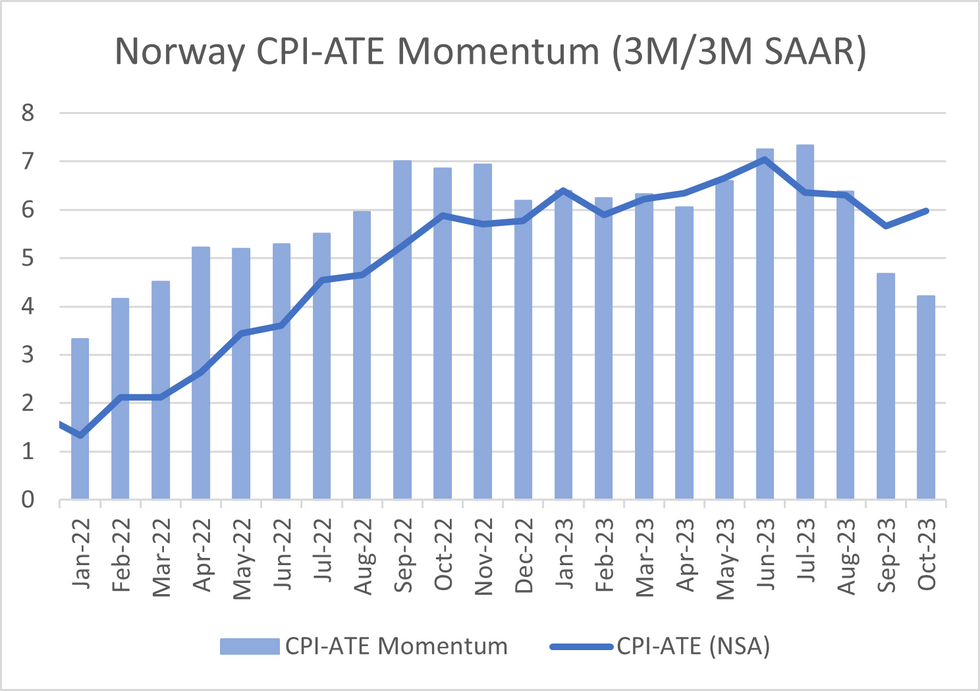

While October's CPI figure was stronger than expected across a broad range of categories, MNI's momentum indices calculated as 3M/3M SAAR show headline and core momentum slowing. Despite this, market and analyst consensus now tilts further towards a 25bp hike at the next meeting - aligned with Norges Bank guidance that "the policy rate will likely be raised in December".

- The lower-than-expected August and September prints mean that CPI-ATE momentum fell to +4.21% 3M/3M SAAR (vs +4.67% prior). However, seasonally adjusted CPI-ATE was still +0.71% M/M (vs +0.16% prior), well above the 2% target on an annualised basis.

- As flagged earlier, Nordea and Handelsbanken have changed their calls for the Norges Bank December meeting, now expecting a 25bps hike to 4.50%. While Handelsbanken note that CPI-ATE is volatile, they still call for a hike when taken alongside the weak NOK and strong wage data.

- JP Morgan maintain their call for a December hold, as they "think core will fall back again in November”.

- Analysts at Citi noted that OIS markets now price around "16bps of hikes for the December meeting (+6bps vs prior)" and the NOK FRA strip has bear steepened on the day, with the Dec23-Mar24 contract up 7.5bps at 4.87% at typing.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok