Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

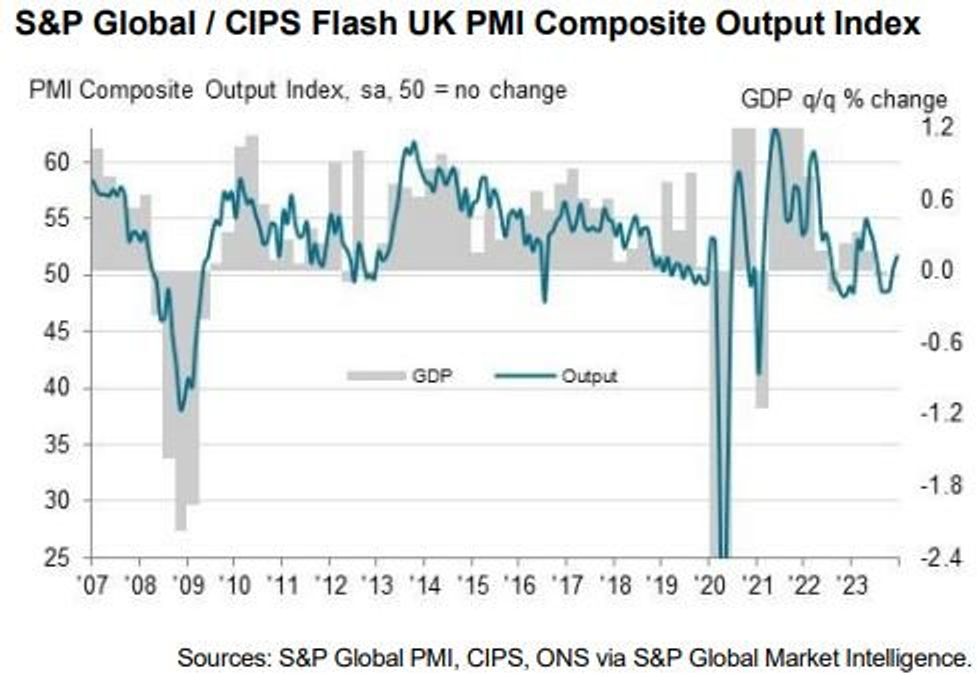

UK December flash PMI readings surprised to the upside overall, with an unexpectedly strong acceleration in the Composite reading to a 6-month high 51.7 (51.0 expected, 50.7 prior).

- That was driven by a jump in Services PMI to 52.7 (51.0 expected, 50.9 prior), helping offset an unexpected dip in Manufacturing PMI to 46.4 (47.5 expected, 47.2 prior), and stood in stark contrast to poor German and French services readings earlier in the session.

- That was the second consecutive month that the PMIs signaled positive private sector output, maintaining a rebound versus the three negative months to October.

- Overall, per the S&P Global/CIPS release, "Higher levels of business activity were supported by a renewed improvement in order books [a rise in new work for the first time since June], alongside efforts to work through post-pandemic backlogs."

- On the Services beat, respondents "again commented on tentative signs of a revival in customer demand, especially for technology and financial services" though "cost of living pressures" and "subdued conditions in the construction sector" were headwinds. In contrast, manufacturing production shrank for the 10th straight month and at a faster pace than in November, with customers described as "overstocked", and backlogs already having been run through to some degree.

- The survey noted staffing numbers falling for the 4th consecutive month, with lower employment in both services and manufacturing.

- Input costs rose to the highest since August, on higher operating expenses (ie salaries) at service sector companies. While output charges also increased robustly though "on average" in Q4, prices charged across the private sector was unchanged vs Q3.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok