Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

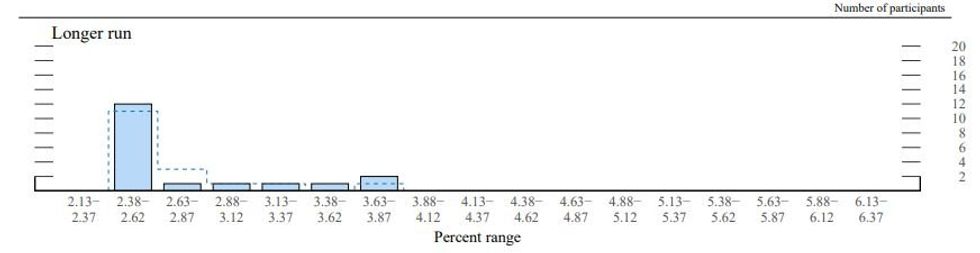

Looking beyond 2024 on the Dot Plot:

- 2025-2026: Compared with the September Dot Plot, the drop-off from 2024’s median to the outer years is likely to be the same or if anything smaller: we see a decent chance they will be unchanged from the last time, at 3.9% for 2025 and 2.9% for 2026, with a similarly wide range reflecting uncertainty about the medium-term outlook.

- The risks here are to the downside though it would be surprising to see anything lower than 3.6% in 2025 and 2.6% for 2026 (the latter converging with the longer-run rate).

- Longer-Run: We’ve seen some analysts highlight that this could finally be the meeting in which the longer-run rate median of 2.5% is raised, with dots in this column having been drifting up in recent projections, and the r-star rate being debated within the Fed. 2.5% is a fairly solid median, with 8 dots at that level and 3 just below it at 2.375%.

- If 2 of those 11 dots were to drift above 2.50% then we would get a median of 2.6% (actually 2.56% unrounded); if 3 were to move higher the median would drift more solidly to 2.6% (2.625%).

- Some analysts expect that this is due a shift higher, with JPMorgan seeing a "good chance" of 2.75%. Even at 2.6% such a move would be considered hawkish as it would be seen as setting a higher limit to future rate cuts.

- Note there are only 18 dots in this column, as the St Louis Fed doesn’t typically participate in this projection.

Source: Federal Reserve September 2023 Projections Of Longer-Run Dot

Source: Federal Reserve September 2023 Projections Of Longer-Run Dot

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok