Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BSP

There is virtual consensus among analysts that the BSP will leave its Overnight Borrowing Rate unchanged at 2.00% at its upcoming monetary policy meeting on Thursday. All of the sell-side analysts surveyed by BBG expect a stand-pat decision, although there some voices suggesting that BSP could lower the reserve requirement ratio (RRR) in the near term.

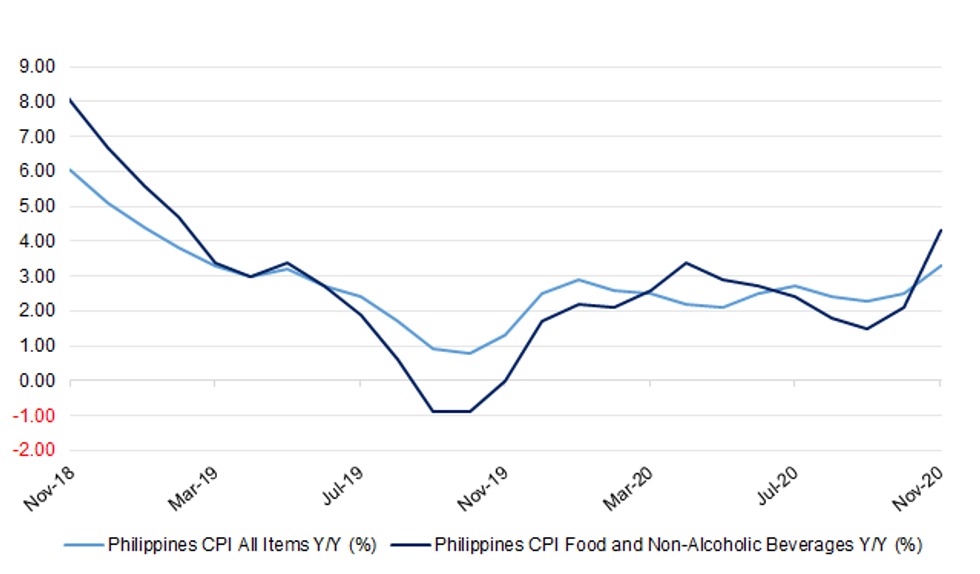

- In the latest data signal, Philippine inflation accelerated more than expected, driven by firmer food prices boosted by a series of typhoons. Headline CPI rose 3.3% Y/Y in November, registering above the mid-point of BSP's inflation target (+3.0% Y/Y +/- 1.0pp) and breaking out of BSP's forecast range (+2.4%-3.2% Y/Y). Gov Diokno commented that inflation is expected to settle within the target range and the impact of typhoons will be transitory.

- Although the BSP unexpectedly lowered its main policy rate by 25bp to 2.00%, BSP Gov Diokno hinted that policymakers may be done with easing for now. He noted that the potential of monetary policy to stimulate economic recovery is limited and argued that the onus is now on fiscal measures to provide support to domestic economy.

- Meanwhile, sluggish transmission of monetary easing has been reflected in a steady deceleration in bank lending growth, which slowed to a 12-year low in October, indicating the limited utility of lowering interest rates.

- There chance of another reduction to the benchmark interest rate this week is very thin, but some analysts noted that BSP could turn to the RRR instead. Currently set at 12%, it easily tops levels seen in regional peers: Indonesia, Malaysia and Thailand. That being said, in the central scenario policymakers will not touch policy levers this time.

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok