Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

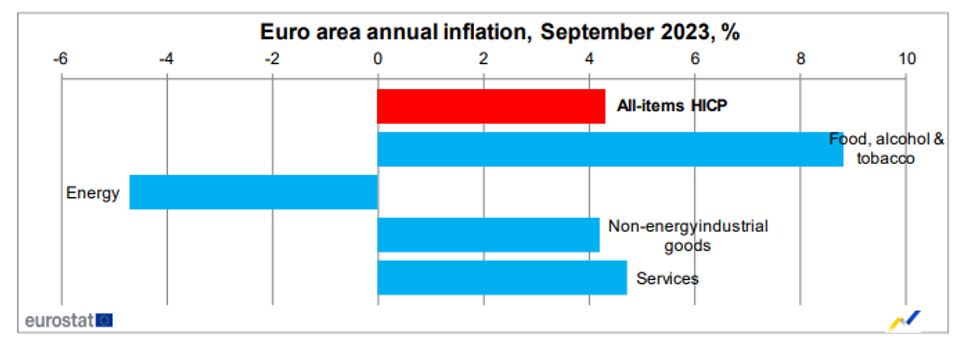

Eurozone flash inflation came in below consensus expectations in September at an unrounded 4.344% Y/Y (vs. 5.2% prior; 4.5% cons). This was the lowest headline print since October 2021.

- The beat was somewhat expected following the national prints released over the last two days.

- Core inflation also came in below consensus - at 4.546% Y/Y (a rounded 4.5% vs 5.3% prior; 4.8% cons), the lowest rate since September 2022.

- The unadjusted monthly prints were 0.331% M/M for headline and 0.248% M/M for core, but we await the ECB's seasonally adjusted series due out later Friday before making sequential assessments.

- The fall in Y/Y core inflation was likely largely driven by the German transport ticket and other statistical / base effects as noted in our preview, but the softer figure versus consensus may reflect more broad based disinflation than was expected. Most of the national-level core CPI data looked softer than expected at first glance, including sequentially - not just Y/Y - for Germany.

- Services inflation diminished to 4.7% Y/Y (vs 5.5% prior), while non-energy industrial goods were 4.2% (vs 4.7% prior).

- We argued in our preview that the September inflation print alone would not be enough to convince the ECB into an October hike even if it came in above consensus, so today's soft print will certainly provide enough ammunition for a hold until December.

- Looking across countries, only two countries - Belgium and the Netherlands - are below the ECB's 2% inflation target, the latter posting a -0.3% Y/Y print this morning. 15 of the 20 Euro-area countries saw the headline rate fall versus August, while 6 of 20 saw sequential monthly falls in prices.

Source: Eurostat

Source: Eurostat

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok