Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

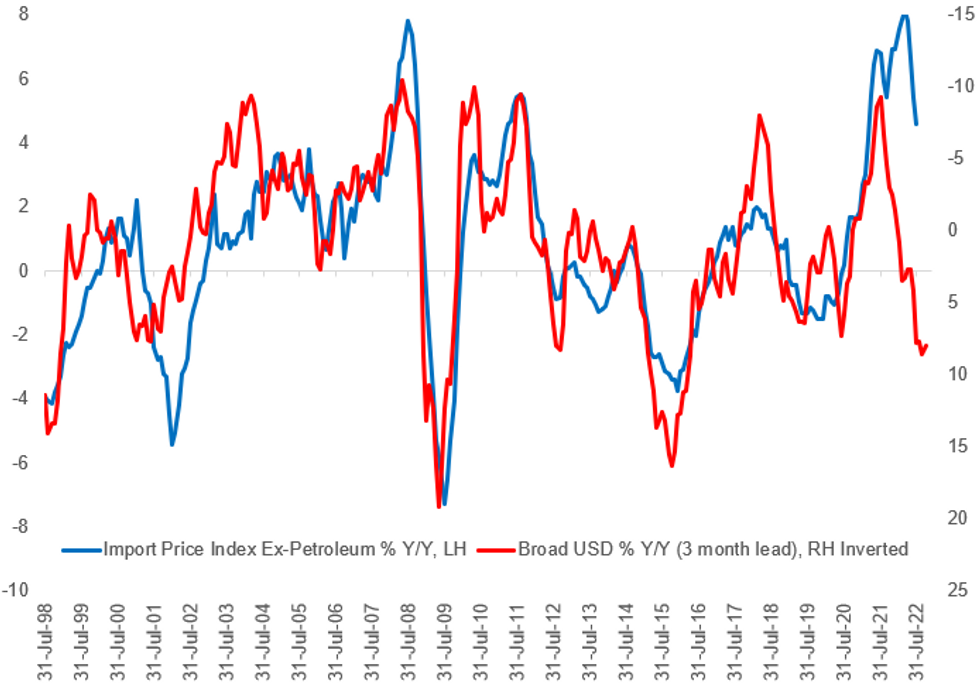

As the weaker-than-expected July import data suggested today, the strong USD will continue to act as a disinflationary force.

- Historically, moves in import prices (ex-petroleum) have corresponded closely to the opposite moves in the USD. On a Y/Y basis, the 8% rise in the broad USD the last 4 months would normally correspond to a Y/Y decline in ex-petroleum import prices of -2%, but the latter has averaged almost +7%.

- Supply chain bottlenecks pushing up global goods prices have been behind much of that discrepancy during the pandemic period, and with those now easing, we would expect Y/Y import prices to recouple with dollar strength and move back toward flat growth by early 2023.

- That should help keep a lid on core goods prices in future CPI readings.

Source: Fed, BLS, MNI

Source: Fed, BLS, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok