Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

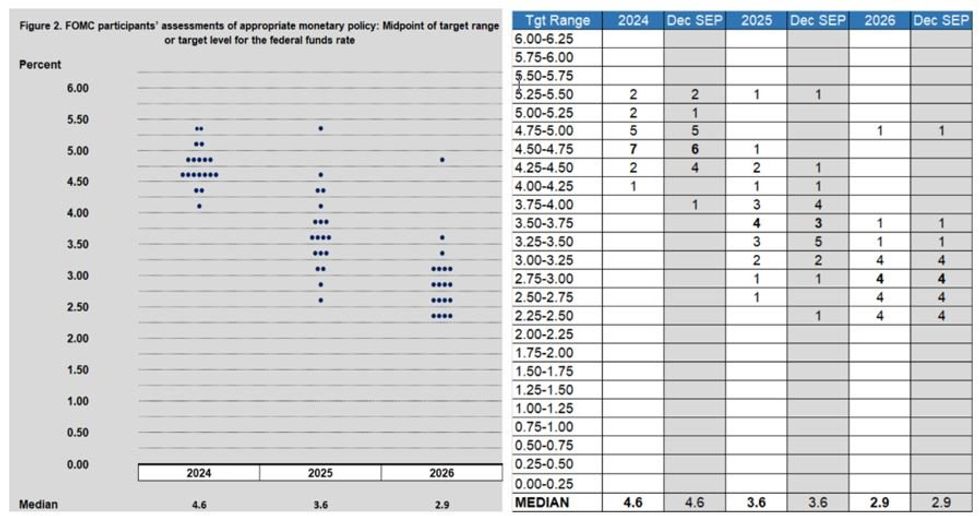

While there is general consensus that the current median dots will persist for all years, including the longer-run dot at 2.5%, the risks are skewed to a higher end-2024 rate and higher longer- run dot.

- In December, 11 of 19 participants posted dots at or below 4.50-4.75% (75bp of cuts), so it would take just two to rise to 4.75-5.00% or higher to move the median up one notch. MNI's Markets Team is pencilling in one net participant moving their dot up beyond 4.50-4.75%, leaving a 10-9 split in favor of 3 cuts.

- However the distribution at the bottom is likely to change, with the low dot (3.75-4.00%) moving up at least one notch, and the number of 4-cutters (4.25-4.50%) reduced from 4 to 2. In other words, the distribution around 2 to 3 cuts should remain fairly solid compared with December (12 of 19 members, vs 11 prior), with the lower end of the distribution shifting higher.

- Our Instant Answers eye both the annual Dot medians as well as the number of participants looking for fewer than 3 cuts (> 4.625%, currently 8 participants) and fewer than 2 cuts (>4.875%, currently 3 participants) to see in the event of a shift up in the 2024 dot whether it is a "solid" hawkish shift (eg 11 or more participants seeing fewer than 3 cuts).

- As for the outer years, we would only anticipate higher dots if 2024 is shifted higher (though some sell-side analysts expect 2024 unchanged but 2025 and 2026 higher).

- And while the submissions for the longer-run dot have been edging higher, this meeting may prove too early for an increase - some analysts expect a rise from 2.5% to 2.6%. There are only 18 longer-run dot submissions (St Louis Fed traditionally doesn't participate), with 8 at 2.50% and 3 at 2.375%; if two of those were to move to 2.625% or higher, the median would rise.

- The MNI Markets Team’s expectations for the updated Dot Plot are below.

Note- one of the 2026 dots is exactly at 2.50%, not midpoint of a range. Source: Fed, MNI

Note- one of the 2026 dots is exactly at 2.50%, not midpoint of a range. Source: Fed, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok