Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

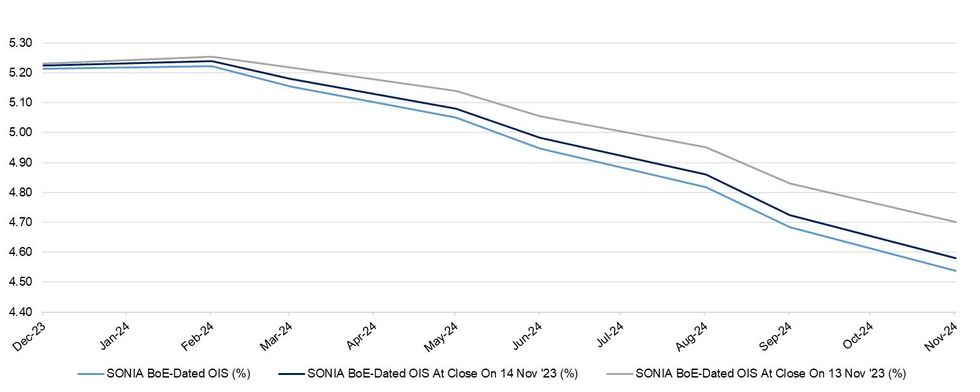

Softer than expected UK inflation data puts a bid into the SONIA strip at the open, although the move is relatively contained, at least in part owing to the size of yesterday’s U.S. CPI-induced rally

- Contracts are off early highs, last showing flat to 5bp firmer through the blues, with the reds outperforming on the strip.

- BoE-dated OIS is also off initial dovish session extremes, but still sits 1-4bp softer on the day.

- A mere ~3.5bp of cumulative tightening is now priced over the next two MPC meetings.

- Beyond there, a 25bp cut is essentially fully priced come the end of the June '24 MPC.

- Dec ’24 BoE pricing now shows ~15bp of additional cumulative cuts vs. pre-U.S. CPI levels, with 3 25bp cuts more than fully priced through '24.

- Comments from BoE hawk Haskel are due at the SONIA futures close.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Dec-23 | 5.214 | +2.7 |

| Feb-24 | 5.223 | +3.6 |

| Mar-24 | 5.154 | -3.3 |

| May-24 | 5.051 | -13.6 |

| Jun-24 | 4.945 | -24.2 |

| Aug-24 | 4.819 | -36.7 |

| Sep-24 | 4.686 | -50.1 |

| Nov-24 | 4.541 | -64.6 |

| Dec-24 | 4.422 | -76.5 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok