Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

The China trade data for October disappointed relative to expectations. Export growth came in at -0.3% y/y, versus +4.5% expected, while imports fell -0.7%, against a flat expectation from the market. The trade surplus was also below consensus, $85.15bn, against a $95.97bn forecast.

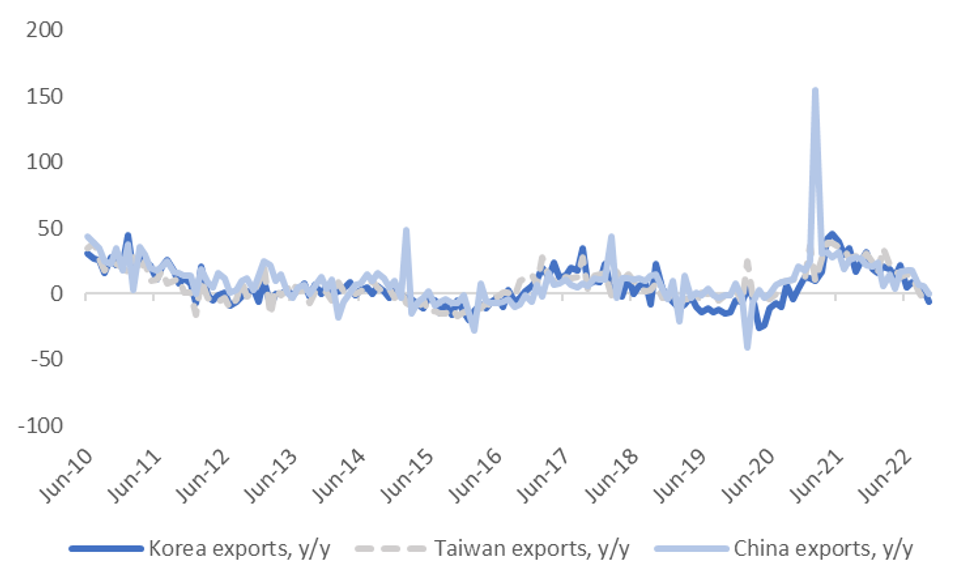

- Export growth has steadily lost altitude through 2022, particularly in recent months, which is in line with trends in other North East Asian economies, see the chart below. This is also the first y/y drop for China exports since the first half of 2020.

Fig 1: Export Growth Trends, China, South Korea & Taiwan, Y/Y

Source: MNI - Market News/Bloomberg

- It complicates the China growth backdrop, as last year and in the first half of this year, exports were performing more strongly. This slowdown is also another sign that the global economy is losing some momentum.

- The weaker import trend suggests the overall domestic demand backdrop remains fairly subdued. The import growth picture has been around flat since March of this year.

- The trade balance miss is only modest, and the underlying surplus position remains intact.

- The market impact from the trade figures has been modest though (little move in the likes of USD/CNH, AUD/USD etc), with higher China/HK equities an offset as market focus remains on potential shift away from CZS.

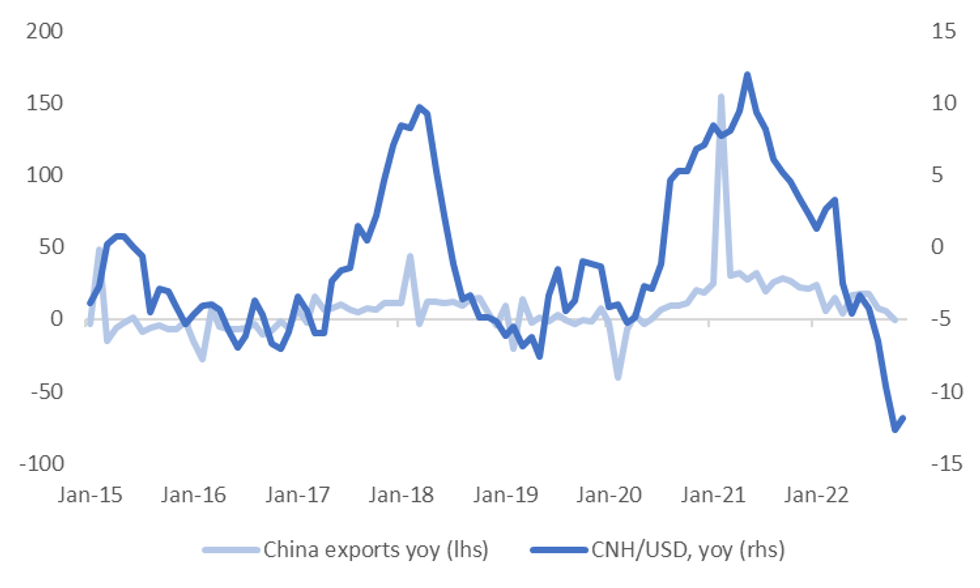

- It's also fair to say weaker CNH levels have priced in a slower export picture, see the second chart below, although this has not been a key driver of CNH trends in 2022 to date.

Fig 2: CNH/USD Y/Y Versus China Export Growth

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok