Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

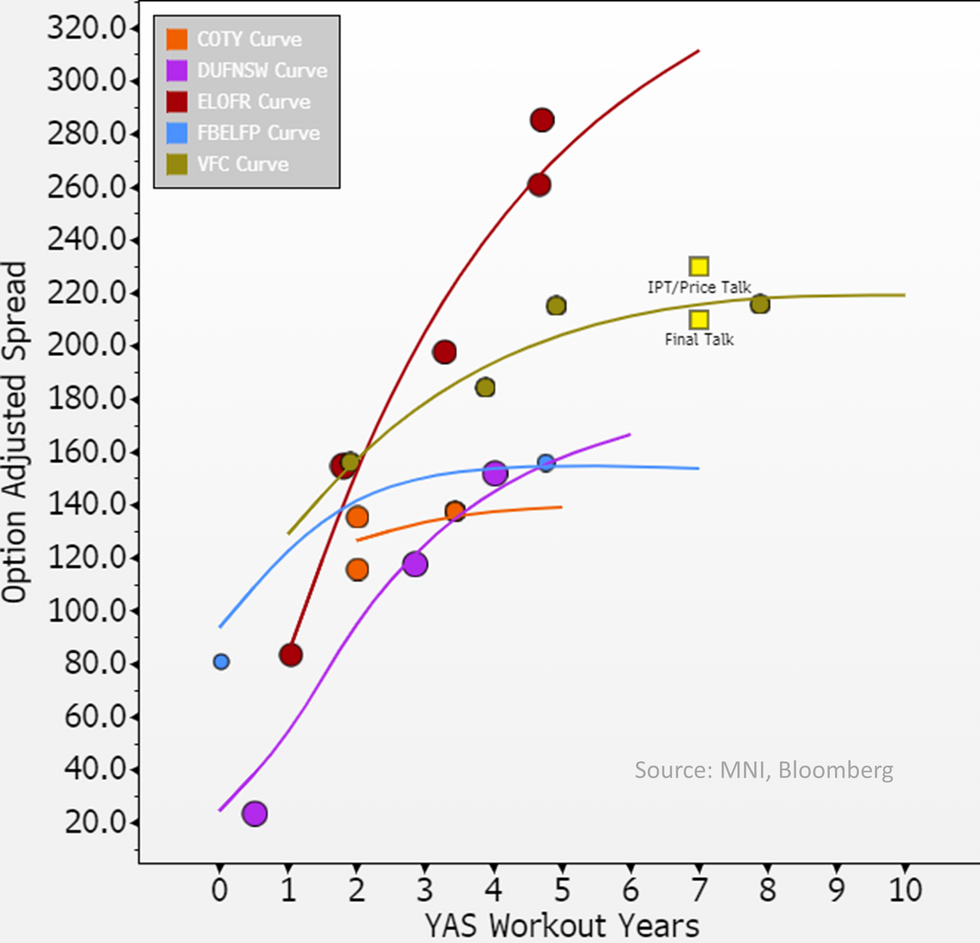

Pricing looks like its giving a ~25bp NIC - flagging ahead of Elo/Auchan FV - both BB rated retailers.

Some differences to note vs. Elo (& explains some of the tightness in Avolta secondary)

- It is predominantly a airport store retailer & hence riding a travel recovery with also firm medium term outlook of +5-7% in organic growth

- No net supply on this deal; it has a tender out on the €24's till next week

- Its coming off double upgrades (now stable) & is still targeting deleveraging (2.6* now vs. 1.5-2* target)

- Public equity, strong analyst coverage (who are in-line with mgmt guidance expecting strong organic rev growth) & double rated

As a aside, the newly issued (& unrated) BEL 29's have moved through the Avolta curve (which was our floor on pricing) - mids currently at MS+146/€100.7 vs pricing at +175/€99.7. As we mentioned before, given less clarity on unrated BEL we prefer Avolta on net balance of risks. BEL did price & still does trade wide of (company reported) fundamentals - on those it's more in line low IG rating (low 100's on spread)

Thoughts on Elo/Auchan to follow.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok