Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

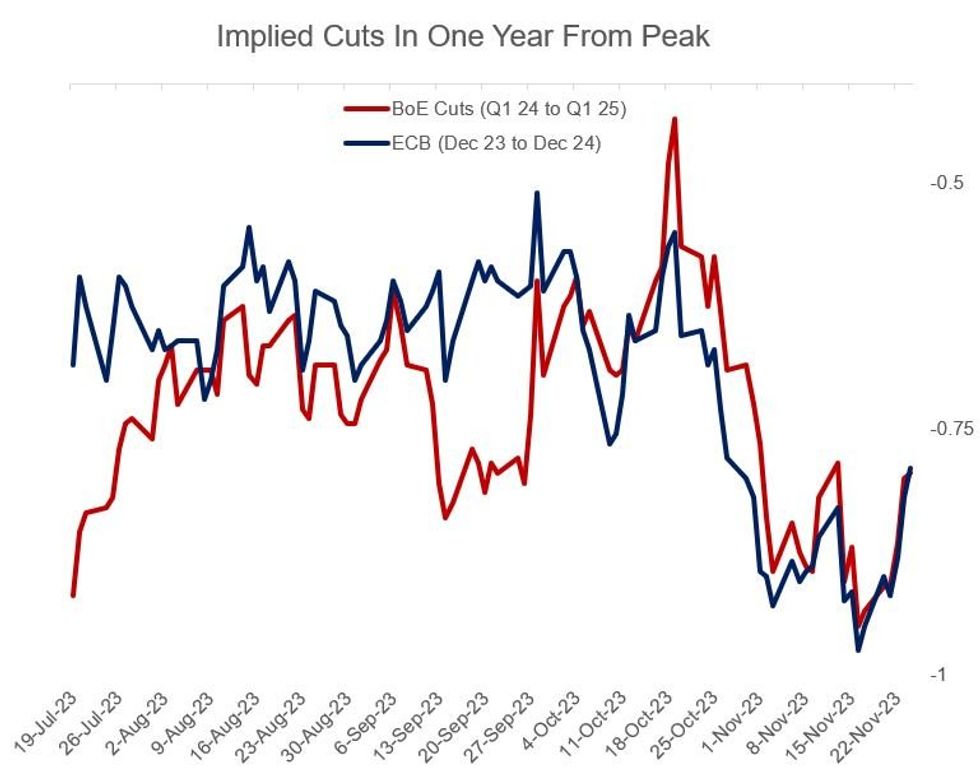

Implied futures pricing for ECB and BoE cuts was pared for the 3rd consecutive session Friday. On the week, around 15bp of ECB cuts and 16bp of BoE cuts have been pared from the implied path a year out from their respective peaks.

- The ECB is seen cutting the depo rate by 79bp between the Dec 2023 peak and Dec 2024, 3bp less than seen Thursday. The first full 25bp cut remains priced cumulatively by the June meeting. While the session had few major flashpoints, ECB speakers reiterated that the fight against inflation is not yet over. On that note, next week brings Eurozone PMIs, arguably the final major input ahead of the ECB's mid-December decision (priced 100% as a hold).

- Meanwhile, a reiteration of hawkish comments from BoE chief economist Pill helped bias BoE-dated OIS in a hawkish direction once again today.

- The BoE is seen reaching its terminal Bank Rate in Feb/Mar 2024, after around 6bp of further tightening (up from the 2-3bp that had been priced earlier this week ahead of stronger-than-expected PMIs and the Autumn Statement). The Bank is then seen cutting 79bp in the 12 months to follow - around 1bp less than seen Thursday. The first full 25bp cut is seen edging into September 2024, vs August as had been seen earlier in the week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok