Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

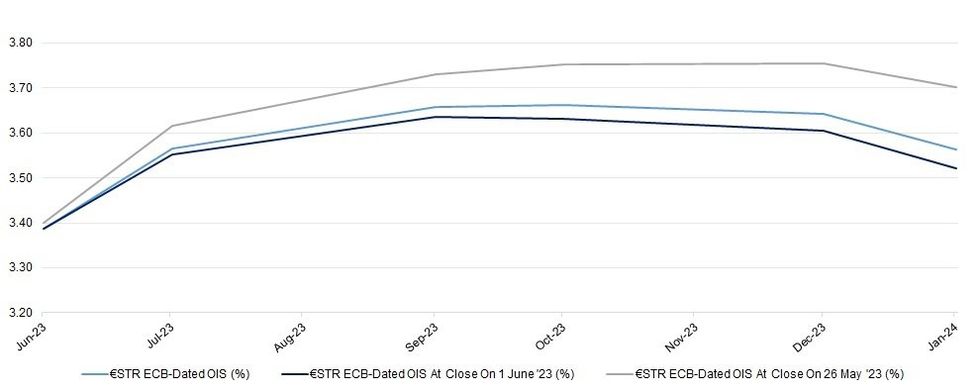

Hope surrounding Chinese property stimulus, firmer Chinese equities and FOMC-dated OIS pricing/U.S. Tsys consolidating a little off Thursday’s dovish extremes leaves ECB-dated OIS pricing flat to ~5bp firmer on the day, with a modest steepening bias evident on the strip.

- Terminal deposit rate pricing sits just above 3.75%, having moved off the recent hawkish extremes on slightly more caveated ECB speak in recent days, FOMC-pricing gyrations and the sharper than expected slowdown in Eurozone CPI (which still resides comfortably above target).

- ECB Executive Board member Panetta flagged that the ECB is not far from terminal rate levels. He went on to note that inflation remains high but stressed that tighter policy will bite more in the coming months. Panetta has always been at the dovish end of the ECB spectrum, and these comments didn’t provide much, if any, tangible market impact.

- Both Panetta & President Lagarde have highlighted the lagged impact of monetary policy within the last 24 hours.

- More recently, Bank of Ireland Governor Makhlouf tipped his hat to the likelihood of 25bp rate hikes in both June & July, although pointed to less clarity beyond that period.

- The impending U.S. NFP print will be a key driver of direction into the weekend.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.386 | +23.9 |

| Jul-23 | 3.565 | +41.8 |

| Sep-23 | 3.657 | +51.0 |

| Oct-23 | 3.661 | +51.4 |

| Dec-23 | 3.642 | +49.5 |

| Jan-24 | 3.564 | +41.7 |

Source : MNI - Market News/Bloomberg

Source : MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok