Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

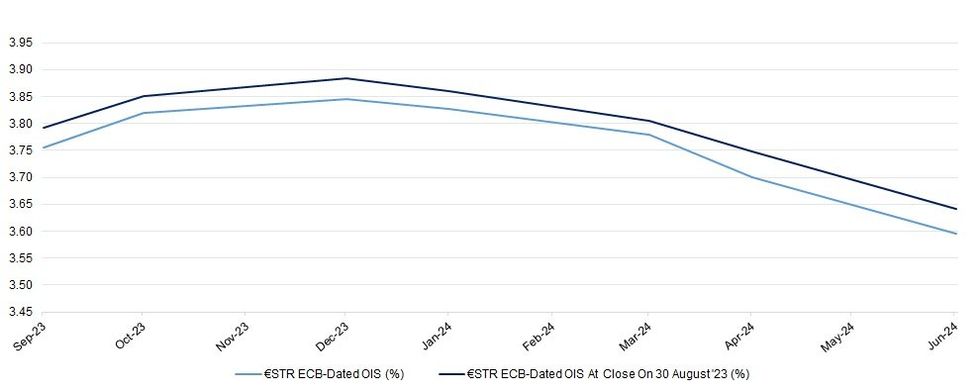

The previously alluded to comments from ECB’s Schnabel have weighed on the ECB-dated OIS strip, with the contracts 3.5-5.0bp softer on the session, as the strip flattens.

- She notes that “under this data-dependent approach, we cannot predict where the peak rate is going to be, or for how long rates will have to be held at restrictive levels. We can also not commit to future actions, meaning we cannot trade off a need for a further tightening of monetary policy today against a promise to hold rates at a certain level for longer.”

- While the comments are not overtly dovish, her historic hawkish bias and lack of commitment to further tightening allows the market to unwind some of the tigthening that was priced into the strip.

- Elsewhere, she flagged a visible moderation in economic activity, alongside stubbornly high price pressures.

- On the hawkish side, she noted that "real risk-free rates have declined back to the level observed at the February Governing Council meeting. This decline could counteract our efforts to bring inflation back to target in a timely manner."

- That leaves ~10.5bp of tightening showing for next month, while terminal deposit rate pricing eases back to 3.94%.

- The ECB debate re: terminal rate level seems to remain within the 3.75-4.00% band, which is reflected in market pricing.

- ECB-dated OIS was already biased a touch lower pre-Schnabel, given activity in the front end of the Euribor strip, with any hawkish flows surrounding firmer than expected French CPI quickly reversed.

| ECB Meeting | €STR ECB-Dated OIS (%) | €STR ECB-Dated OIS At Close On 30 August '23 (%) |

| Sep-23 | 3.756 | 3.7916 |

| Oct-23 | 3.819 | 3.852 |

| Dec-23 | 3.846 | 3.8836 |

| Jan-24 | 3.828 | 3.8605 |

| Mar-24 | 3.779 | 3.8052 |

| Apr-24 | 3.700 | 3.7482 |

| Jun-24 | 3.596 | 3.6416 |

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok