Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

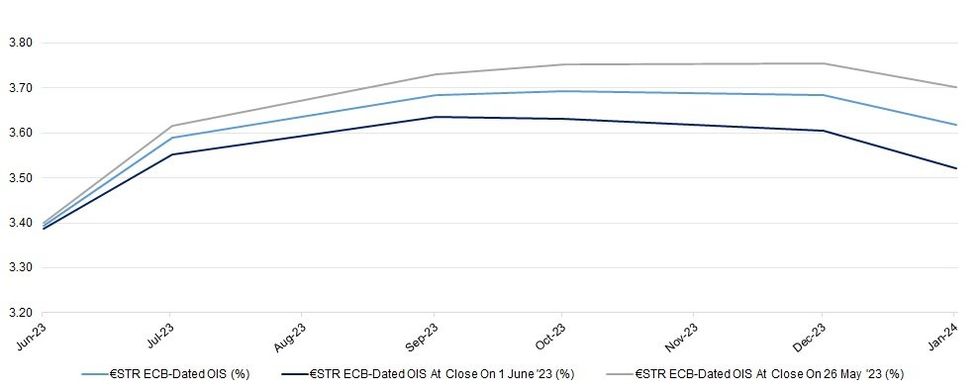

Global impulses continue to bias ECB pricing higher at the start of the new week, with weekend musings from Bank of Italy Governor Visco and a mark lower in the final Eurozone services PMI (to a still more than healthy 55.1) doing little to influence the space, as cheapening in core global FI markets and higher oil prices are noted.

- That leaves a 25bp hike virtually fully priced for the June meeting, while terminal rate pricing of just below 3.80% (in deposit rate terms) is seen come October. While we have recovered from the post-CPI data troughs seen last week, we are not back to the levels observed at the close of business for the week prior.

- In terms of specifics, Visco conceded that current monetary policy settings are correct, although indicated that he would have preferred a more gradual approach. This underscored his position at the dovish end of the ECB spectrum, although he did caution that underlying inflation may take some time to moderate.

- Elsewhere, Croatian central bank chief Vujcic noted that wage pressures are “still very lively” while highlighting that risks to inflation remain to the upside.

- Comments from President Lagarde and Bundesbank chief Nagel round off today’s scheduled ECB communique.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.393 | +24.5 |

| Jul-23 | 3.589 | +44.1 |

| Sep-23 | 3.685 | +53.7 |

| Oct-23 | 3.692 | +54.4 |

| Dec-23 | 3.684 | +53.6 |

| Jan-24 | 3.618 | +47.0 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok