Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

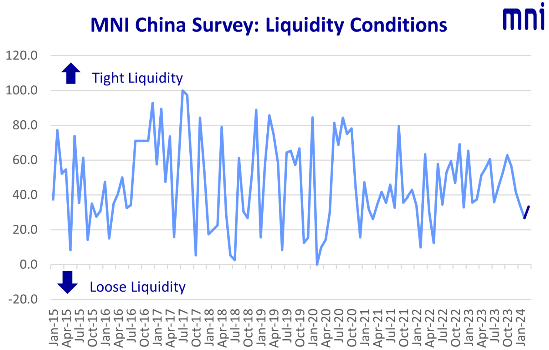

The People’s Bank of China net-drained liquidity for the first time in 15 months as authorities stepped up action to address so-called “idle funds”, which are used for arbitrage with little benefit to the real economy, the latest MNI Liquidity Conditions Index showed.

Liquidity conditions though remained reasonable. Traders concerns’ over a lack of demand in the economy persisted despite some bright spots in February’s data releases.

The central bank is now prioritising improving capital operation efficiency and preventing idle funds and arbitrage issues, a senior trader in Beijing told MNI, but others stressed conditions remained ample despite the authorities’ move.

The MNI China Liquidity Condition Index stood at 33.3 in March, up from February’s 22-month-low of 26.8. The higher the index the looser conditions.

The PBOC conducted CNY387 billion in MLF in February, draining CNY94 billion after offsetting a maturities of CNY481 billion, the first net drain since November 2022. The PBOC also drained net CNY467 billion via open market operations as of March 25, MNI calculated.

To soothe market reactions, the PBOC later clarified that it still aimed to keep liquidity ample, whilst Deputy Governor Xuan Changneng told MNI “all parties are greatly concerned by the issue of idle funds circulating in the financial system,” at a recent press conference.

The central bank is likely to prioritise channelling liquidity towards the real economy, rather than having it cycle through the banking system pushing up leverage or flowing into property and equity markets, PBOC experts recently told MNI. (See MNI: PBOC Easing More Likely In H2 After Potential Fed Cut)

DEMAND INSUFFICIENT

The MNI China Economy Condition Index slipped to 54.8 in March, down from 56.1 in February, with a Guangdong-based trader noting domestic demand remained weak despite good export and investment data in January and February.

“Recent indicators show the economy is not so robust, with weak domestic demand, I think monetary policy will loosen further, probably in Q2,” a Beijing trader said.

To stabilise the recovery China will increase off-the-book special government debt issuance and extend maturities to raise funds for medium- and long-term growth initiatives, while considering additional revenue sources for local governments to ease their fiscal challenges, a prominent policy advisor told MNI. (See MNI: China To Extend Debt, Reform Local Gov Tax, MNI: China 5% GDP Growth Depends On Land Revenue)

RATES

The MNI China 7-Day Repo Rate Index climbed to 54.8 in March, with 35.7% of the participants expecting an increasing rate given the end-quarter MPA and authorities focusing on increasing fund efficiency.

The MNI China 10-year CGB Yield Index read 32.1, with 42.9% of traders predicting the yield would drop given expectations of further rate cuts and increased demand for treasury bonds.

SPECIAL QUESTION

For this month’s survey, MNI asked “do you expect a further MLF cut in the next three months?” with 57.1% of respondents seeing a strong likelihood while 19.0% said it was unlikely.

The People’s Bank of China is likely to reduce its policy rates to boost total social financing and support credit demand as it moves to stoke greater core inflation in line with Beijing’s monetary policy direction, a senior policy advisor told MNI in an interview. (See: MNI INTERVIEW: PBOC To Cut Rates To Boost Credit - Zhang Bin)

Click below for the full report:

MNI China Liquidity Index March 2024.pdf

For full database history on the MNI China Liquidity Index™, please contact:sales@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.