Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

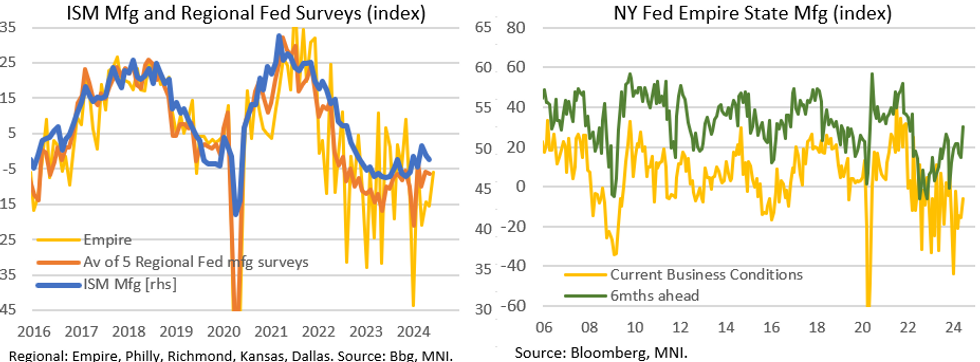

The NY Fed's Empire State Manufacturing index came in a little stronger than expected in June at -6.0 (-10.0 expected, -15.6 prior). This was the biggest monthly increase since November 2023, to the least-negative reading since February 2024.

- The Empire survey, while historically volatile, on balance represented a positive start to June's round of regional Fed manufacturing readings. While activity continues to contract, the survey provided signals that pronounced 2Q weakness may have represented a trough in activity in New York State for now.

- The positive signals included: Prices Paid slipped to the lowest since January (24.5) after four relatively elevated months, with prices received dipping slightly, suggesting softening inflation pressures. New Orders jumped by 15.5 points to -1.0, the best reading since July 2023, Shipments turned positive after 3 months of contractions, and expectations for activity 6 months ahead rose by 15.6 points to 30.1, the highest since March 2022.

- On the other hand, some indicators in the survey were softer: hiring remained weak (the number of employees index slipped 2.3 points to -8.7, near the post-pandemic lows), while capex expectations remained 2.0 for a 2nd consecutive month, both joint-lowest since May 2023 and among the weakest readings outside of a declared recession.

- Supply availability, which was available in this report for the first time, was -1.0, indicating little change (this was firmly negative in the backdated series through early 2022 amid global supply chain problems).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok