Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

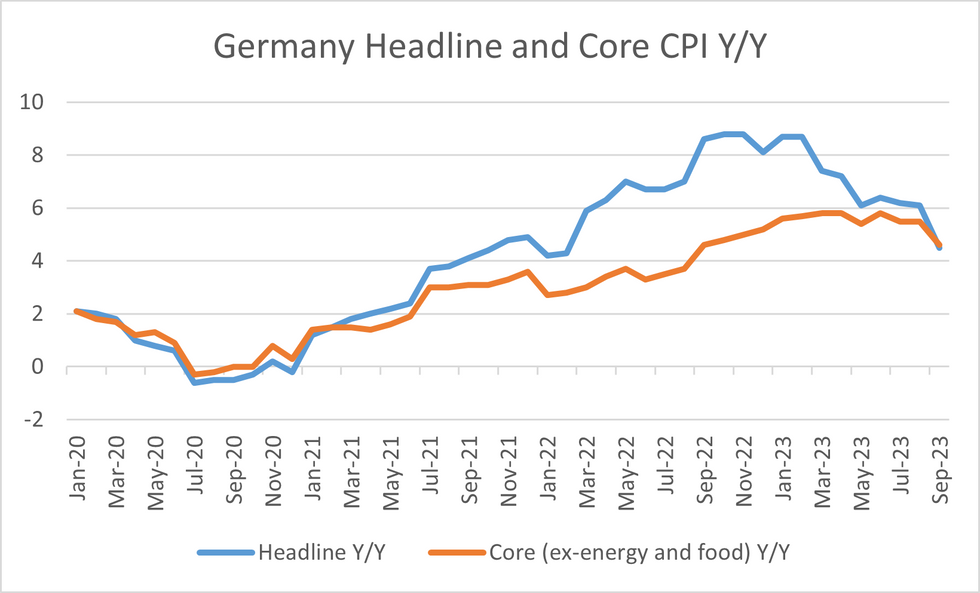

A dovish reaction in Bunds there to that prelim September HICP reading which came in at 4.3% Y/Y vs 4.5% expected (the 4.5% CPI was right in line with MNI's state-level based estimate, as did core CPI at 4.6%).

- There's no core HICP estimate released in the prelim data but there may have been some encouragement in sharp drop in goods inflation to 5.0% Y/Y from 7.1% Y/Y in August - the collapse in energy prices, again on base effects, to 1.0% Y/Y from 8.3% prior, will have done much of the heavy work in that disinflation. Food prices slipped to 7.5% Y/Y from 9.0%. Ex-food and energy goods inflation looks to have been well below 4% Y/Y, a sign of improving core dynamics overall.

- We knew that Services prices would slip sharply Y/Y on transport base effects and it did, to 4.0% Y/Y from 5.1% prior.

- Overall while we await monthly SA data for Germany the overall disinflation trend after the high base effects of the summer appears to be going more or less as expected.

- The Eurozone-wide figures out Friday are likely to come in below expectations set before today's Spanish / Belgian / German prints.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok