Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMANY

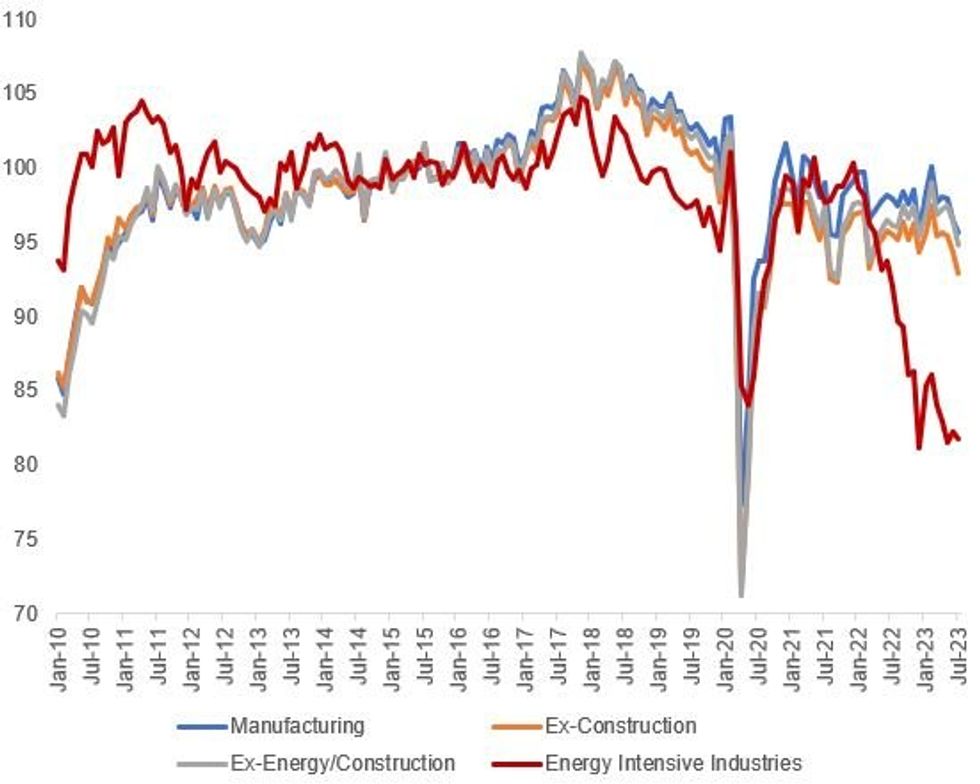

Factory orders act as a barometer of demand and are a leading indicator - the weak July industrial production data released this morning confirmed ongoing weakness in output however.

- July IP came in at -0.8% M/M (-0.4% survey, -1.4% prior) and -2.1% Y/Y (in line with survey; -1.5% prior). This was the third straight month of decline.

- And when excluding energy and construction, production was -1.8% M/M (energy production was +2.2% and construction +2.6%), and -1.3% Y/Y - suggesting that "core" industries are even weaker than the headline figures suggest.

- Energy-intensive industries, from chemicals to metals fabrication, remain in crisis - after ticking 1.0% M/M higher in June, this area pulled back 0.6% in July and production sits 18% below end-2021 levels (and 3% below pandemic lows for that matter).

- The most energy-intensive sectors represent around 17% of industrial value added but 3/4 of industrial energy consumption (as of 2021 per Destatis) and show no signs of improvement.

- The German government is beginning to eye structural reforms, but these will come too little and too late. Demand is clearly waning on all fronts, from domestic sources, intra-eurozone, and from abroad.

- As such German industrial production looks like it will get worse before it gets better, which poses downside risks to the 0.0% Q/Q GDP outturn expected for Q3 (same as Q2) and generally bodes ill for the Eurozone outlook in H2 2023.

Source: Destatis, MNI

Source: Destatis, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok