Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MARKET INSIGHT

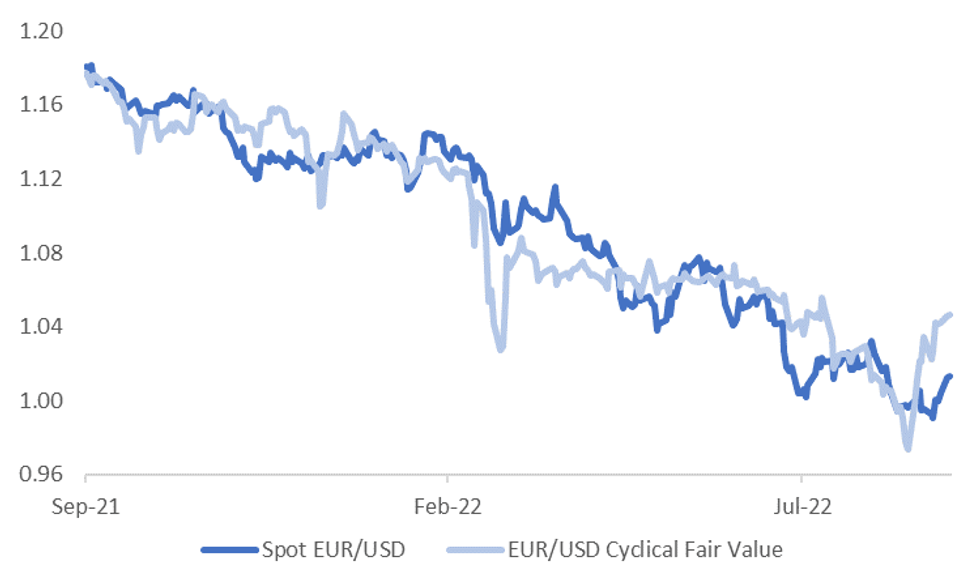

At face value, the EUR/USD rebound looks to have further to run. The first chart below plots spot EUR/USD against a simple cyclical fair value metric. The fair value metric is made up of the EU-US 2yr swap rate differential and the Citi relative terms of trade indices for the two blocs.

- The current fair value estimate sits above 1.04, versus current spot at 1.0130. The improvement in the fair value in recent weeks reflects higher swap rate differentials and a turnaround in the relative terms of trade outlook (albeit from depressed levels).

- Note the fair value regression is based off the past year of data and has an R^2 of 87%.

Fig 1: EUR/USD Still Below Simple Simple Cyclical Fair Value

Source: Citi/MNI - Market News/Bloomberg

Source: Citi/MNI - Market News/Bloomberg

- Interestingly though, recent correlations suggest the relative terms of trade back drop is a more important driver of EUR/USD, rather than yield differentials. A trend that has been evident in other parts of 2022 as well.

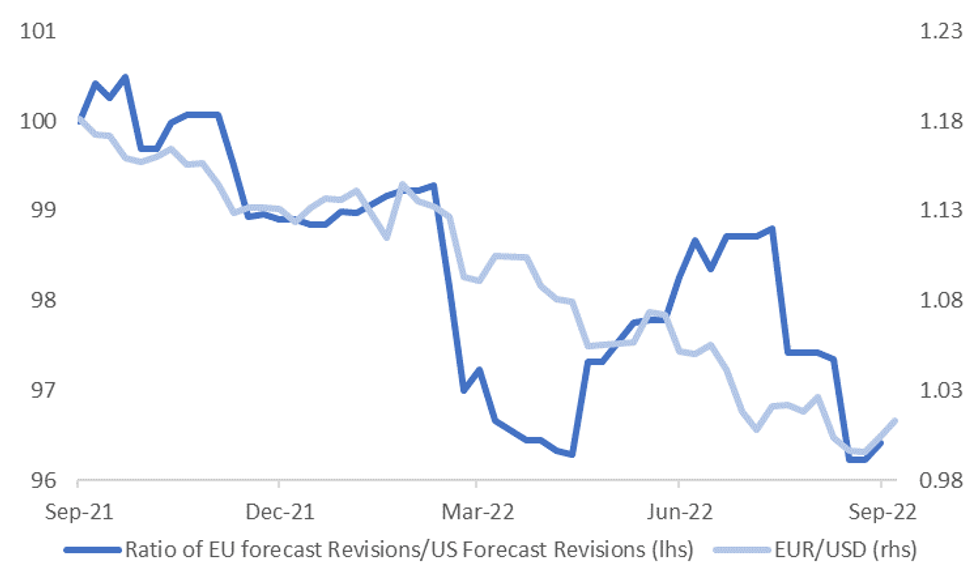

- This is closely linked with another key driver of the EUR/USD outlook, relative growth prospects between the EU and US. The second chart below overlays EUR/USD against the ratio of EU growth revisions to US growth reversions, sourced from J.P. Morgan.

- Not surprisingly, J.P. Morgan economists have revised down their EU growth projections more than the US, most notably in recent months. This has been the broader trend from other economists as well.

- The potential for an energy supply induced recession in the EU area certainly can't be discounted as we approach year end. A further sharp downward revision to the EU growth outlook, relative to the US, would weigh on the EUR/USD rebound, all else equal.

- On this basis, the market may be reluctant to take EUR/USD quickly back to the implied level of short term fair value, particularly ahead of the northern hemisphere winter.

Fig 2: EUR/USD Versus Relative J.P. Morgan Growth Revisions (EU to US)

Source: J.P. Morgan/MNI - Market News/Bloomberg

Source: J.P. Morgan/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok