Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

South Korea's Nov trade figures were better than expected. Export growth rose 7.8% y/y (5.0% forecast and 5.1% prior). Imports fell more than expected -11.6% y/y (forecast -8.6%). This left the trade surplus much higher than projected at $3.8bn ($1bn forecast and $1.63bn prior).

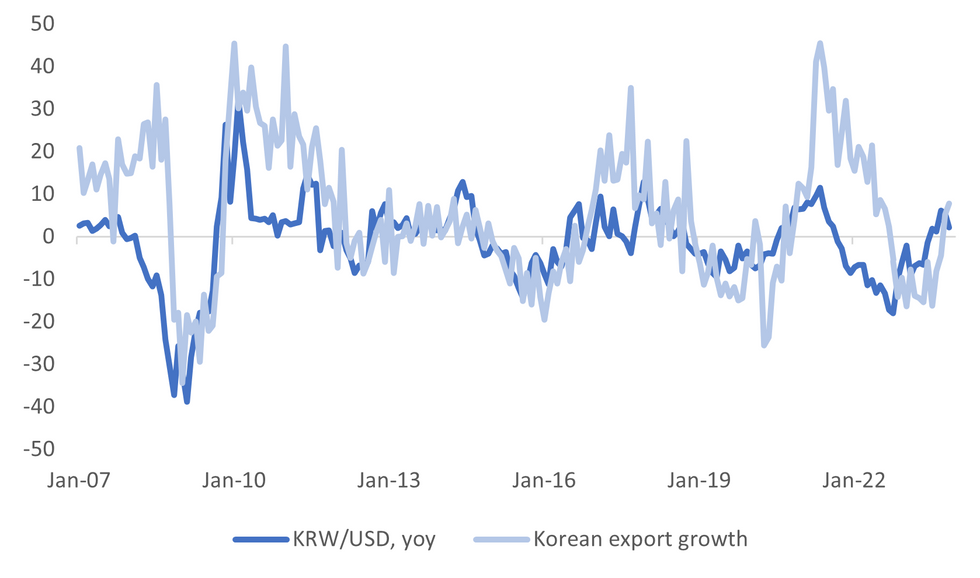

- This is the firmest pace of export growth, in y/y terms, since mid 2022. Won gains, in y/y terms are trailing the improved trend, but only at the margin, see the chart below.

- Export in m/m terms rose 1.3%, against a 0.80% gain in October.

- Chip exports ended their run of y/y falls, rising 12.9% (aided by base effects). Car exports remained strong, up 21.5%, while battery exports rose 24.8%.

- By country, exports were down 0.2% y/y to China, but this has been on improving trend. Export growth to the US remained positive.

- Today's data, coupled with the Nov PMI, moving back to 50 (from 49.8), provides some modest optimism around the growth backdrop as we move into 2024.

Fig 1: South Korean Export Growth & KRW/USD Y/Y Changes

Source: MNI - Market News/Bloomberg

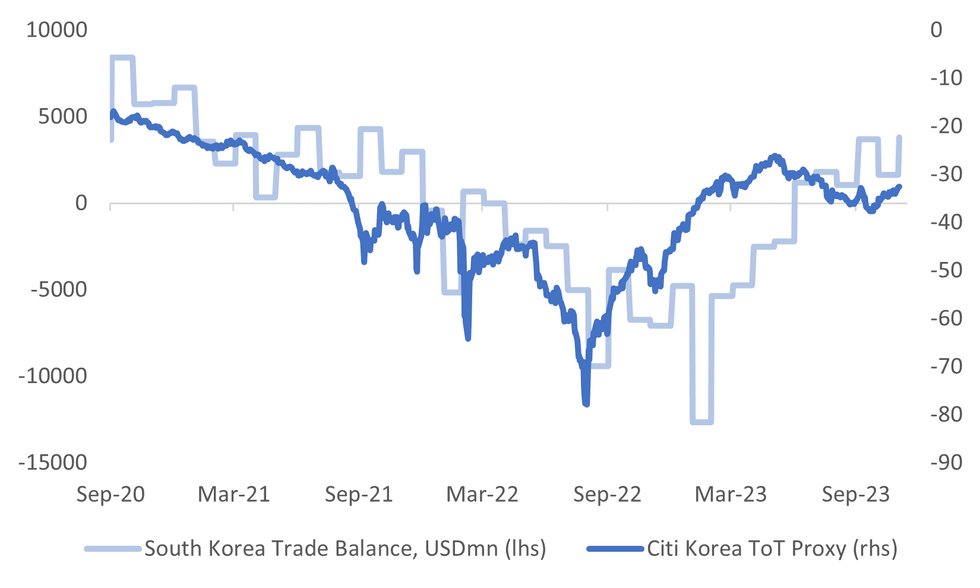

- The trade surplus beat, aided by the import drop, is consistent with some recent improvement in the terms of trade proxy (CITI), see the second chart below. The surplus is at fresh highs back to Q3 2021.

- The won is only marginally firmer in 1 month NDF terms, post today's prints, last near 1297 (+0.10%).

Fig 2: South Korea Trade Position & Citi Terms Of Trade Proxy

Source: CITI/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok