Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

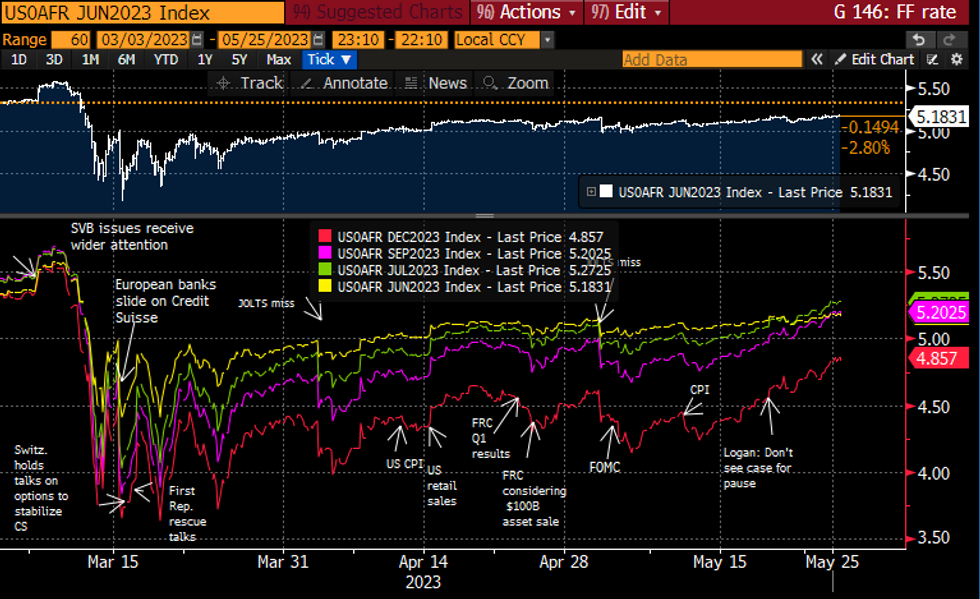

- Fed Funds implied rates are slightly off fresh post-regional banking woe highs having reversed a dip after the FOMC minutes. Of note, the terminal effective sits around 5.27% with the July decision and with 42bp of cuts from the peak to year-end for less than one full 25bp cut priced from current levels.

- Cumulative change from 5.08% effective: +10bp Jun (-0.5bp), +19bp Jul (-1bp), +11.5bp Sep (unch), -4bp Nov (+1bp), -23bp Dec (+2bp), -41bp Jan (+3bp).

- Bostic (’24 voter) spoke late yesterday, possibly mildly more hawkish than recently by noting that the “best case” is the Fed won’t mull rate cuts until well into 2024. Continued data dependency isn’t particularly different to Monday saying he’s comfortable waiting a bit to see how things play out and that policy acts with a lag.

- Ahead, Barkin (’24 voter) and Collins (non-voter, with text). Barkin spoke Mon (won’t pre-judge June policy decision) and before that May 16 (willing to raise raises again if necessary) whilst Collins last spoke in March.

Source: Bloomberg

Source: Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok