Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

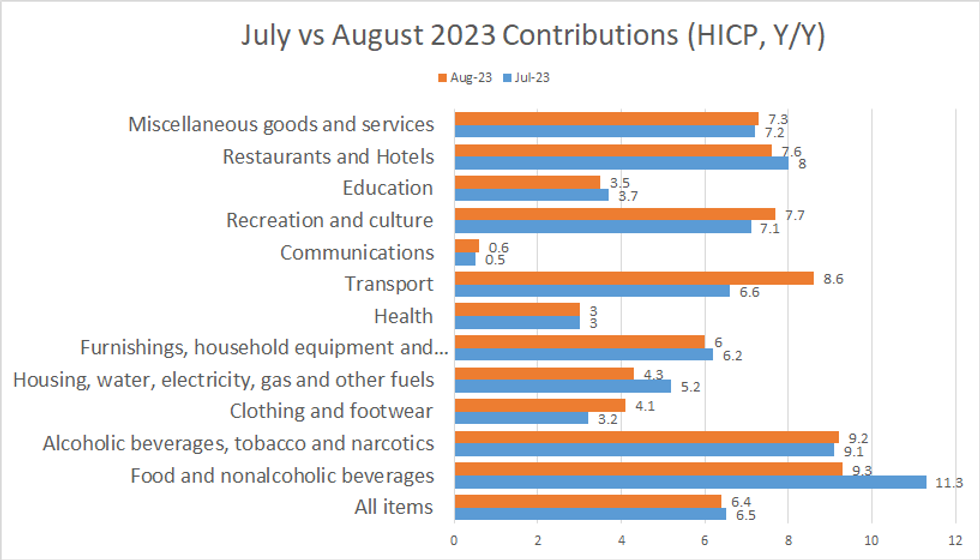

Germany final inflation prints for August printed in line with flash readings. Headline CPI was +6.1% Y/Y and +0.3% M/M, while HICP was +6.4% Y/Y and +0.4% M/M.

- Core CPI printed 5.5% Y/Y for the second consecutive month (decelerating to 0.3% M/M from 0.4% in July, not seasonally adjusted).

- Final readings for core HICP series and special aggregates (energy, non-energy industrial goods, services) have not yet been released but likely also fell in line. The basically unrevised release would imply core HICP (ex-energy, food, alcohol and tobacco) confirmed at +6.3% Y/Y and +0.3% M/M - a 0.4pp sequential disinflation from the July print of +0.7% M/M but 0.1pp higher from 6.2% Y/Y.

- Notable HICP sub-component prints were:

- Electricity prices +15.5% Y/Y (vs +13.9% prior). As noted in our Inflation Insight for August, energy price rises were driven by base effects of a government energy relief package last year.

- Transport services +37.6% Y/Y as the final month of the 9-Euro transport ticket base effects push up core, the ending of which should contribute to significant September disinflation. A monthly fall in air and sea fares (-8.7% M/M and -8.4% M/M) meant transport services fell -2.5% M/M overall.

- Package holidays saw a sequential monthly step down to +1.6% M/M (vs 10.9% prior). The end of summer should reduce the impact that this components has on core inflation, following its large weighting change this year (1.5% of HICP basket in 2023 vs 0.7% in 2022).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok